Stock-Market Rally Nearing Inflection Point After Wall Street’s ‘Fear Gauge’ Surge

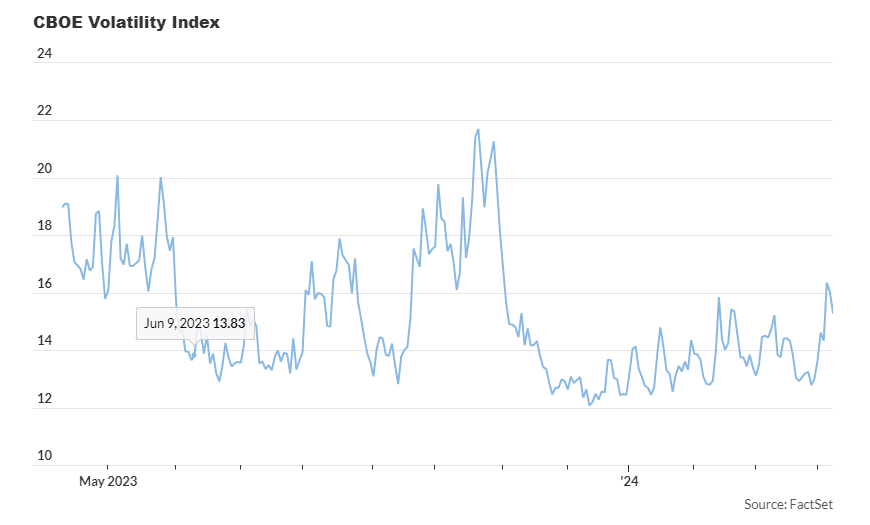

Analysts are cautioning that the recent rise in the Vix, along with heightened interest in bearish options, suggests potential weakness ahead for stocks. Following a tranquil period of five months, the stock market’s upward momentum encountered a disruption last week as the Vix, commonly referred to as the “fear gauge,” surged, raising concerns among some experts about a more significant downturn. The Cboe Volatility Index, or Vix, has raised alarms about the possibility of a stock market correction, defined as a decline of 10% or more from recent peaks. Its notable 23% increase last week, the most significant weekly surge since September, pushed the index above 16 for the first time since November 1, according to FactSet data. This surge follows an extended period of subdued Vix readings, attributed to various factors such as the growing popularity of short-term option contracts and derivative-income exchange-traded funds. Analysts warn that this uptick in volatility could gather pace as traders unwind derivative positions that thrive on market stability. The Vix measures implied volatility based on options market activity, with volatility typically accelerating during market downturns. The combination of a climbing Vix and increased demand for bearish put options indicates to Tyler Richey, co-editor of Sevens Report Research, that the market may be approaching a “tipping point,” suggesting potential softening in the weeks ahead. Richey suggests a scenario akin to the selloff experienced between late July and late October of the previous year. Last week’s surge in demand for bearish put options propelled the 10-day rolling average of the Cboe equity put-call ratio to its highest level since January 26, signaling heightened interest in options tied to individual stocks. Furthermore, the uptick in demand for out-of-the-money puts compared to calls has drawn attention. This surge, according to Charlie McElligott, a derivatives strategist at Nomura, has led to a notable increase in the options-market skew, indicating a shift in investor sentiment. Historically, rapid increases in skew from historically low levels have coincided with weak excess returns for stocks. These indicators suggest potential near-term challenges for markets, especially with upcoming economic data releases and Treasury auctions that could impact bond yields. Slow-moving catalysts such as a strengthening economy and evolving expectations regarding Federal Reserve policies also contribute to market uncertainty. While some analysts caution against overinterpreting last week’s volatility, they acknowledge the vulnerability of the recent market rally. Despite mixed performance on Monday, with the S&P 500 and Dow Jones slightly down while the Nasdaq edged up, low trading volume indicated investor distraction, possibly due to external events like the total solar eclipse. However, the Vix finished lower on Monday, showing a decline of 5.1%, reflecting ongoing market uncertainty despite the recent surge in volatility. The remarkable rally in stocks since late October, without significant pullbacks, underscores the unusual resilience of the market in recent months. John PaulJohn Paul is the founder of DayTradeToWin, a trading education and software company established in 2008, supporting traders worldwide. His expertise focuses on price action-based futures trading strategies and structured market analysis. DayTradeToWin delivers trading education, indicators, and software tools designed to help traders apply disciplined, rule-based decision-making across global futures markets. He is the creator of multiple trading methodologies, including the Sonic System, Atlas Line, and Trade Scalper, which help traders identify structured opportunities in markets such as the E-mini S&P 500 (ES), Nasdaq (NQ), crude oil (CL), and gold (GC). Official website: https://daytradetowin.com daytradetowin.com