U.S. stock index futures displayed strength in the early hours of Thursday, with a stable bond market and close attention on two key factors: the release of August’s retail sales data and the debut of ARM Holdings’ IPO.

The performance of stock-index futures at the time was as follows:

- S&P 500 futures (ES00, 0.34%) saw a rise of 10 points, equivalent to a 0.2% increase, reaching 4527.

- Dow Jones Industrial Average futures (YM00, 0.23%) gained 45 points, or 0.1%, to hit 34963.

- Nasdaq 100 futures (NQ00, 0.41%) added 44 points, marking a 0.3% uptick, and reaching 15596.

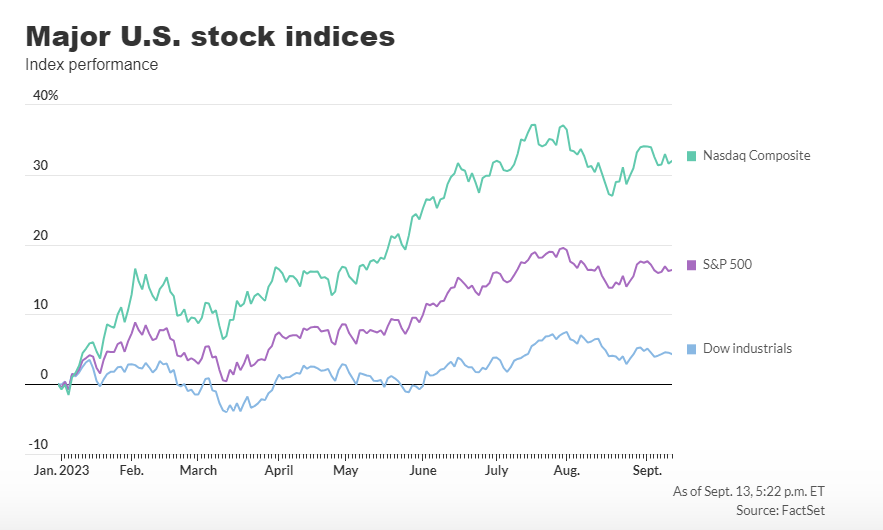

In the prior trading session, the Dow Jones Industrial Average (DJIA) slipped by 70 points, translating to a 0.2% decrease, closing at 34576. Meanwhile, the S&P 500 (SPX) managed to eke out a 6-point gain, representing a 0.12% uptick and closing at 4467. The Nasdaq Composite (COMP) saw an increase of 40 points, or 0.29%, closing at 13814.

Market sentiment appeared cautiously optimistic on Thursday’s early trading session as declining government bond yields indicated reduced concerns about the Federal Reserve’s potential interest rate hikes, especially after the latest inflation data. A report from the previous day showed that annual core consumer prices, excluding volatile elements like food and energy, had increased by 4.3% in August, down from the previous month’s 4.7%, marking the lowest level in nearly two years.

Henry Allen, a strategist at Deutsche Bank, noted, “Following much anticipation, the markets largely shrugged off the U.S. CPI release yesterday. Bonds and equities remained fairly stable before eventually experiencing a bond rally.”

At present, the market was pricing in a minimal probability of the Federal Reserve increasing borrowing costs following its upcoming meeting next week. The likelihood of a 25 basis point hike in November remained uncertain and would depend on forthcoming releases, including August producer prices and retail sales data, both scheduled for 8:30 a.m. Eastern Time. Additionally, other U.S. economic updates set for Thursday included the release of weekly initial jobless benefit claims at 8:30 a.m. and July business inventories at 10 a.m.

Investors were also closely monitoring the initial trading of ARM Holdings (ARM) following the pricing of its IPO at $51 per share, which was positioned near the upper end of the anticipated range. This valuation gave the U.K.-based company a market capitalization of $52 billion. A well-received ARM IPO was expected to potentially reinvigorate the IPO market and enhance overall bullish sentiment.

Susannah Streeter, head of money and markets at Hargreaves Lansdown, commented, “Given the enthusiasm among investors, it appears that ARM could have sought an even higher price. However, the company seems to be taking a cautious approach to ensure a surge in the share price once trading commences.”

Another significant event for the day was the policy decision by the European Central Bank (ECB), scheduled for 2:15 p.m. Frankfurt time and 8:15 a.m. Eastern Time. While ECB decisions typically have a limited impact on U.S. markets, it was unusual for a major central bank meeting to be approached without a clear market consensus. The ECB faced a two-in-three chance of implementing a 25 basis point interest rate hike, as it grappled with persistent inflation and slowing economic activity, particularly in Germany.

John Paul is the founder of DayTradeToWin, a trading education and software company established in 2008, supporting traders worldwide. His expertise focuses on price action-based futures trading strategies and structured market analysis.

DayTradeToWin delivers trading education, indicators, and software tools designed to help traders apply disciplined, rule-based decision-making across global futures markets.

He is the creator of multiple trading methodologies, including the Sonic System, Atlas Line, and Trade Scalper, which help traders identify structured opportunities in markets such as the E-mini S&P 500 (ES), Nasdaq (NQ), crude oil (CL), and gold (GC).

Official website: https://daytradetowin.com