Attractive Valuations for the S&P 500 Could Spell Trouble for Future Returns

Markets took a breather on Wednesday as attention shifted from geopolitical tensions to upcoming economic data, interest rate expectations, and tariff developments. With a busy slate of economic reports due over the next two days, investor sentiment may shift quickly.

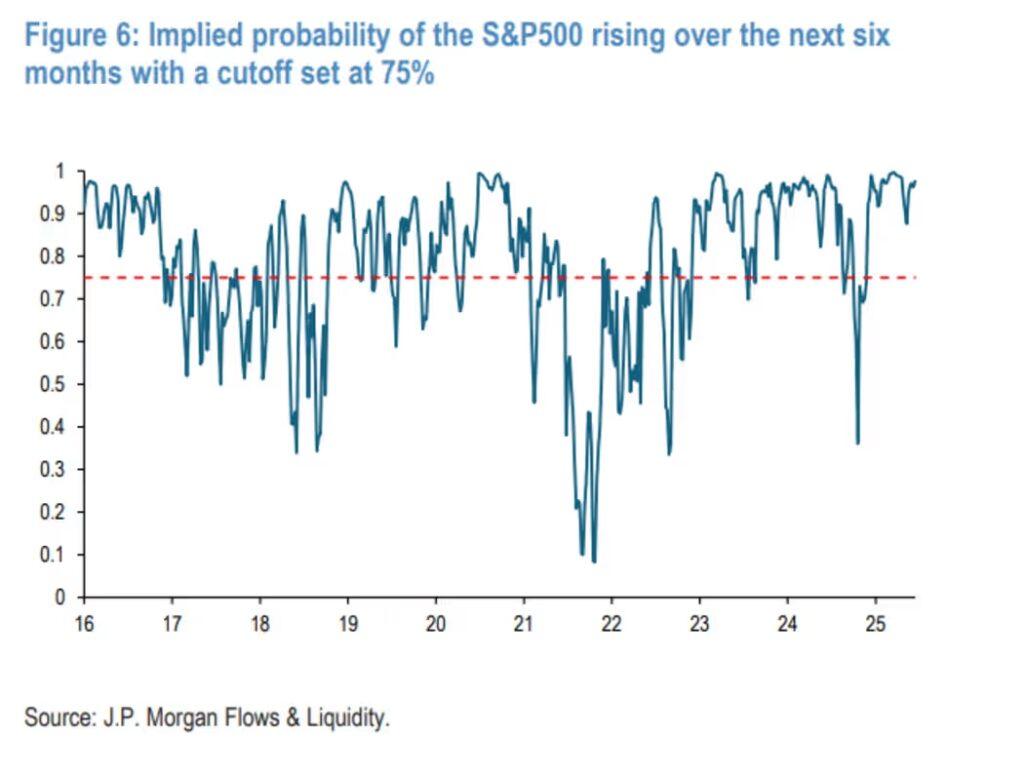

But economic indicators aren’t the only thing guiding markets. Strategists at JPMorgan, led by Nikolaos Panigirtzoglou, have developed a six-month forecasting model for the S&P 500 that incorporates six signals: volume, valuation, investor positioning, fund flows, economic momentum, and price momentum. Each factor is measured relative to its historical average using z-scores.

Trained on data through late 2022 and tested with more recent figures, the model prioritizes predicting downturns—since simply being long equities would have been correct over 90% of the time. In testing, the model accurately predicted market declines 76% of the time in its training sample and 63% of the time in out-of-sample data—significantly outperforming other models, which tended to miss downside risks.

Among its insights:

- Stronger economic momentum (reflected in global manufacturing PMI trends) and higher trading volume increase the odds of a market rally.

- Overcrowded bullish positioning and large inflows into equity funds vs. bonds raise the risk of a pullback.

- Excessive equity momentum relative to bonds is another warning sign.

The most surprising takeaway? Attractive valuations often precede weaker returns. The strategists suggest this is because valuations are closely tied to shifts in the 10-year Treasury yield—so when yields fall, it may be a signal of economic weakness ahead.

Despite that, the model’s current reading is optimistic: it sees a 96% chance the S&P 500 will rise over the next six months.

John Paul is the founder of DayTradeToWin, a trading education and software company established in 2008, supporting traders worldwide. His expertise focuses on price action-based futures trading strategies and structured market analysis.

DayTradeToWin delivers trading education, indicators, and software tools designed to help traders apply disciplined, rule-based decision-making across global futures markets.

He is the creator of multiple trading methodologies, including the Sonic System, Atlas Line, and Trade Scalper, which help traders identify structured opportunities in markets such as the E-mini S&P 500 (ES), Nasdaq (NQ), crude oil (CL), and gold (GC).

Official website: https://daytradetowin.com