Tariff Risks Are Rising—But Markets Aren’t Paying Attention

Stocks look set for a subdued session, even as warning signs build beneath the surface. Tuesday’s bond market reaction to hotter-than-expected June inflation showed just how quickly sentiment can shift—especially as tariffs start to play a bigger role.

Consumer prices jumped last month by the most since early 2025, and some economists are starting to connect the dots. Henry Allen, macro strategist at Deutsche Bank, says investors remain too relaxed about the inflation outlook.

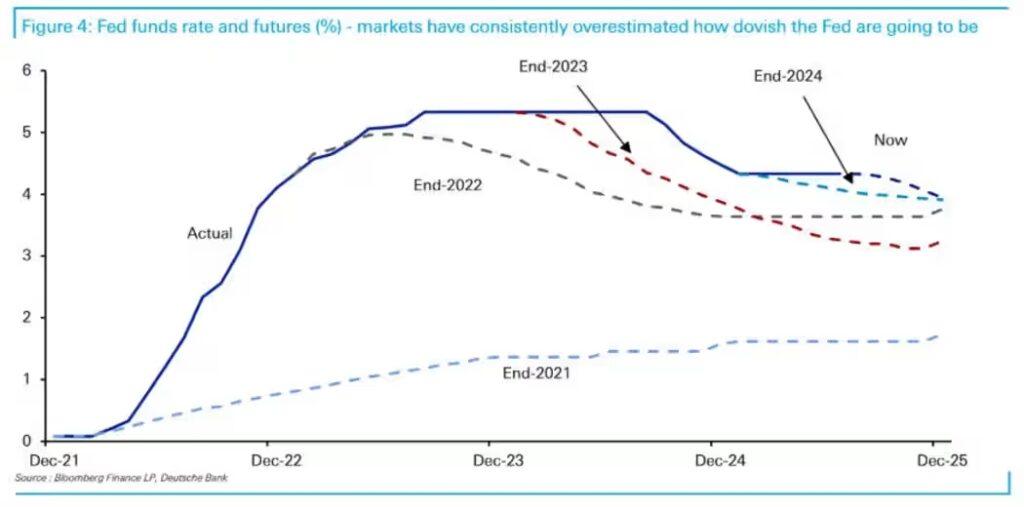

“There’s still a striking complacency across major asset classes,” Allen said in a Wednesday note. “This is now the fourth consecutive year that markets have misjudged how hawkish the Fed would actually be.”

One key factor Allen flags: rising tariffs. Former President Donald Trump has proposed sweeping trade policies, including a 10% baseline tariff on most imports, with additional levies on steel, aluminum, autos, and possibly copper. Markets, however, haven’t priced in these possibilities.

According to betting markets, there’s a 28% chance Trump’s proposed 30% tariff on EU goods becomes reality, and a 43% chance that Canada’s 35% tariff goes through. “If enacted, they’d be a major surprise,” Allen said. “Most investors aren’t prepared for them.”

Beyond the U.S., retaliation is also a risk. The European Union reportedly has a list of U.S. products ready to target in response to new duties. Allen warns this could ignite a broader inflation wave by disrupting global supply chains and pushing prices higher.

Evidence may already be emerging. Tuesday’s inflation data showed the largest-ever monthly jump in household appliance prices. Allen believes this could signal a broader trend: “The strength in core goods may soon spread across the consumer basket, making inflation more persistent.”

Geopolitical risks could add fuel to the fire. Allen cites last month’s Iran-Israel tensions, which briefly drove oil prices higher, as the kind of unpredictable shock that can reignite inflation expectations.

Meanwhile, central banks are still expected to cut rates later this year—bets that Allen says are increasingly out of touch. “Markets keep assuming dovish pivots that never arrive. At the start of 2025, traders were pricing in a Fed rate cut by June, which didn’t happen.”

Debt burdens could also play a role. Governments may be tempted to tolerate surprise inflation as a short-term fix for high debt, even if markets eventually demand higher rates to compensate.

“The bottom line,” Allen said, “is that markets continue to underestimate the inflation risks still ahead—particularly from tariffs. That could set the stage for yet another round of painful surprises.”

John Paul is the founder of DayTradeToWin, a trading education and software company established in 2008, supporting traders worldwide. His expertise focuses on price action-based futures trading strategies and structured market analysis.

DayTradeToWin delivers trading education, indicators, and software tools designed to help traders apply disciplined, rule-based decision-making across global futures markets.

He is the creator of multiple trading methodologies, including the Sonic System, Atlas Line, and Trade Scalper, which help traders identify structured opportunities in markets such as the E-mini S&P 500 (ES), Nasdaq (NQ), crude oil (CL), and gold (GC).

Official website: https://daytradetowin.com