Jefferies: Fed Cuts May Spark Shift Away from Big Tech

The S&P 500 fell 1.6% on Friday—its worst session since May—after soft jobs data and renewed tariff concerns rattled markets. But U.S. stock futures on Monday hint at a partial rebound, and some strategists remain optimistic despite near-term headwinds.

According to Jefferies, investors now face a roughly seven-week period marked by a weakening labor market and limited central bank support. The Fed is widely expected to cut interest rates by 25 basis points at its September 17 meeting, lowering the target range to 4.00%–4.25%.

Still, Jefferies remains positive. “It’s a tougher sell after this week, but we still believe equities are heading higher,” they wrote over the weekend. Strong second-quarter earnings are one reason: two-thirds of S&P 500 companies have reported so far, and 85% have beaten expectations—lifting earnings forecasts and supporting stock prices.

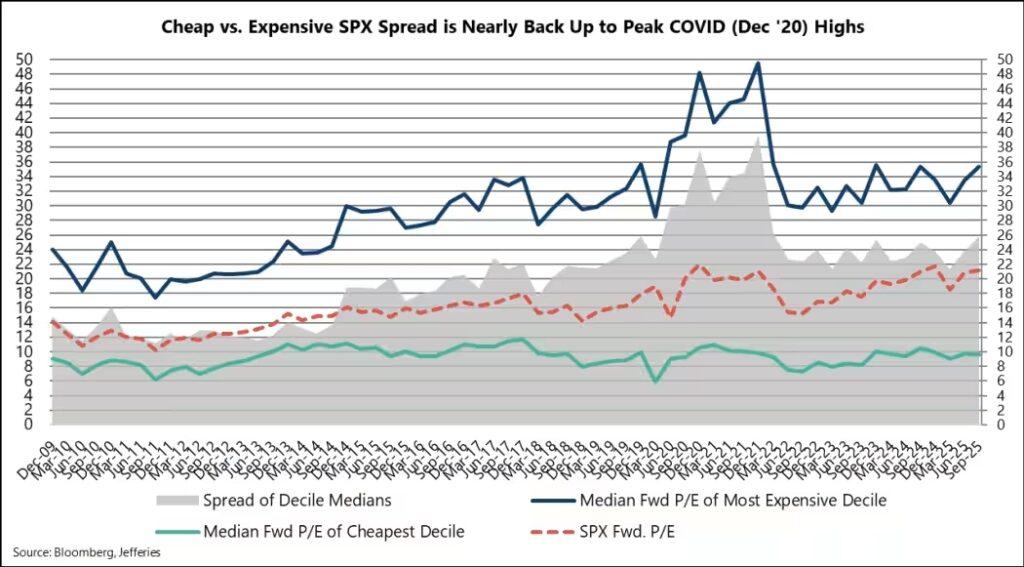

But Jefferies is growing cautious on Big Tech. The sector now makes up a record 44% of the S&P 500 by weight—surpassing the 2000 dot-com peak. While still delivering solid results and acting as a defensive play, Jefferies questions how much longer that leadership can last.

They’re not calling it a bubble, but note that valuations are stretched. The premium on tech versus the cheapest stocks is in the 87th percentile historically—making the trade look “long in the tooth.”

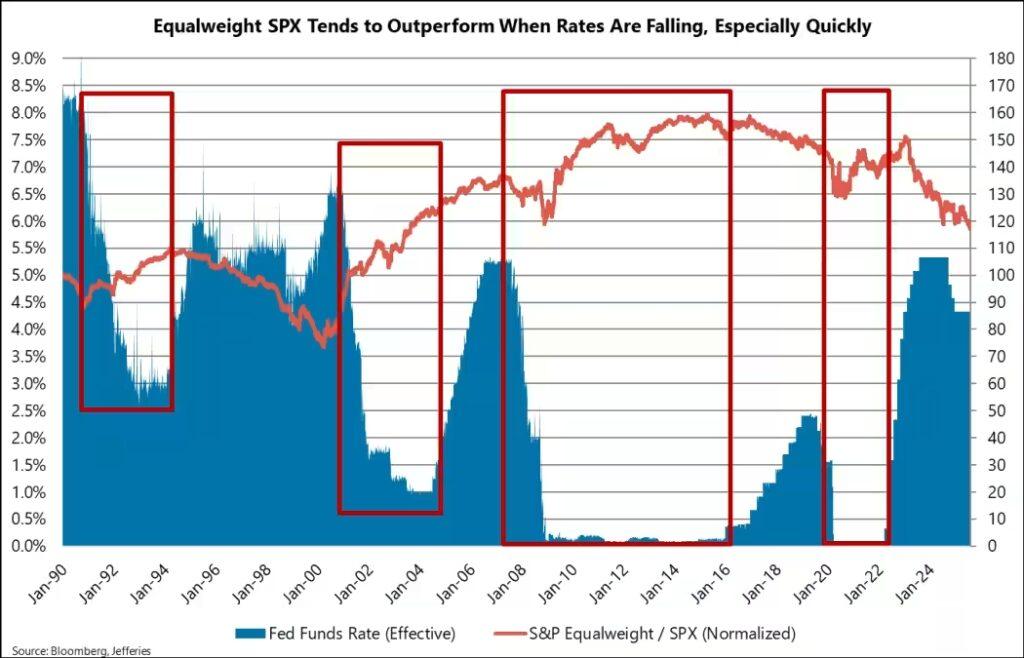

More importantly, Jefferies notes that rate cuts tend to favor the equal-weighted S&P 500, which gives more influence to smaller names outside tech. Historically, most periods of outperformance for equal-weighted stocks have come when the Fed is easing policy.

“We’re not predicting a major tech selloff,” Jefferies says. “But with the Fed turning dovish, history suggests a rotation may be starting. Friday’s payroll data could be the signal: it might finally be time to shift out of large-cap tech.”

John Paul is the founder of DayTradeToWin, a trading education and software company established in 2008, supporting traders worldwide. His expertise focuses on price action-based futures trading strategies and structured market analysis.

DayTradeToWin delivers trading education, indicators, and software tools designed to help traders apply disciplined, rule-based decision-making across global futures markets.

He is the creator of multiple trading methodologies, including the Sonic System, Atlas Line, and Trade Scalper, which help traders identify structured opportunities in markets such as the E-mini S&P 500 (ES), Nasdaq (NQ), crude oil (CL), and gold (GC).

Official website: https://daytradetowin.com