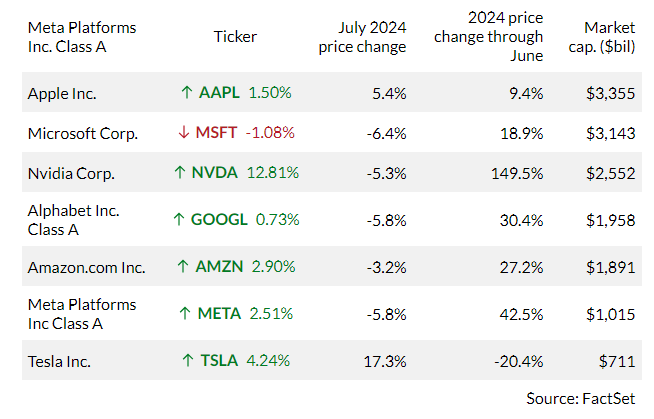

A rate cut isn’t expected in the coming week, but the Fed could provide insights on whether small-caps can maintain their winning streak. A significant market influence might soon impact the rapidly evolving stock market. U.S. equities experienced notable volatility last week as investors dealt with a sharp selloff in big-tech stocks and a rotation into small-cap and value stocks. This shift from large to small stocks, known as the “Great Rotation,” has been a key market trend in July. This transition was somewhat expected. The so-called Magnificent Seven stocks had an impressive start to the year, with Nvidia Corp. (NVDA) rising nearly 150% in the first six months of 2024, and Meta Platforms Inc. (META) up over 42%. Their rise boosted major stock indexes but also resulted in unusually narrow market breadth. The pendulum was ready to swing the other way, and the recent tech selloff was a reflection of that shift. The Magnificent Seven stocks corrected, pulling down indexes like the S&P 500 (SPX) and Nasdaq Composite (COMP), which are heavily weighted towards technology stocks. In contrast, the Russell 2000 (RUT), which tracks small-cap stocks, gained 10.2% over the past 12 trading days, outperforming the S&P 500 by 13.3% — its largest 12-day outperformance ever, according to Dow Jones Market Data. It also outperformed the Nasdaq Composite by 17.1%, its second-largest 12-day outperformance of the Nasdaq. On Friday, the Russell 2000 logged a 3.5% weekly gain, surpassing the performance of the major equity indexes. Dave Sekera, chief U.S. market strategist at Morningstar, commented, “This correction over the past week or two has been very healthy. It indicates a rotation where we’re seeing a big move out of AI names, large-cap growth stocks, tech stocks, and into value stocks and smaller-cap stocks.” While large drops can be alarming, the high valuations of megacap stocks have become increasingly hard to justify. Investors saw this when Alphabet announced its earnings beat, yet the stock still dropped 5%. Emily Roland, co-chief investment strategist at John Hancock Investment Management, explained, “The earnings weren’t bad, but they had to be amazing to justify the run-up we saw in prices.” The momentum of this trend could hinge on next week’s big event — the July FOMC meeting. What to Watch for in the Fed Meeting The Federal Open Market Committee is set to meet on July 30 and 31. While no rate cuts are expected, investors will closely monitor for indications of when the Fed might start reducing interest rates. Rate changes impact the economy in various ways, especially for small-cap versus large-cap companies. Smaller companies, more reliant on business loans, tend to be more sensitive to rate fluctuations. Thomas Martin, senior portfolio manager at GLOBALT Investments, noted, “Rate cuts benefit small-caps as their variable-rate financing and operating expenses decrease, potentially boosting earnings. Lower rates can also stimulate the economy, increasing customer spending.” Investors began moving from megacap to small-cap stocks before the first rate cut of this cycle, suggesting small-caps could gain even more momentum when rates start to drop. Martin believes the Great Rotation could continue to some extent. “It’s a recalibration, getting things back to a more reasonable relationship among different market parts,” Martin said. “Diversification remains key; it’s not about shifting entirely from growth to value.” The dual nature of rate cuts — potentially stimulating the economy but also signaling a need for stimulation — will be closely watched. Investors will pay attention to Fed Chair Powell’s comments on the economy’s health. Sekera stated, “I suspect we’ll hear increased confidence that inflation is on the downward path, allowing for future rate cuts. I’ll also be listening closely for Powell’s economic outlook.” If the Fed signals the economy is slowing, it could aid the inflation battle but raise recession risks. Small-cap companies, less insulated from downturns, are more sensitive to a slowing economy. Roland at John Hancock remarked, “The Fed is aiming for a soft landing, but it’s tricky. Small cracks in the labor market and economy could prompt rate cuts.” Investors will be keenly watching the Fed’s assessment of the economy during the FOMC meeting to gauge the likelihood of a soft landing. Last week, the Dow (DJIA) ended on a high note, advancing 1.6% on Friday and about 0.8% over the week. The S&P 500 (SPX) and Nasdaq Composite (COMP) also gained on Friday but ended the week with losses. The S&P 500 was down 0.8% for the week, and the Nasdaq was down 2.1%. The Dow, however, finished a consecutive four-week winning streak. Aside from the FOMC meeting’s conclusion on Wednesday, traders will be watching job openings on Tuesday, ADP employment numbers on Wednesday, and the U.S. unemployment rate on Friday to assess the labor market and overall economic strength. John PaulJohn Paul is the founder of DayTradeToWin, a trading education and software company established in 2008, supporting traders worldwide. His expertise focuses on price action-based futures trading strategies and structured market analysis. DayTradeToWin delivers trading education, indicators, and software tools designed to help traders apply disciplined, rule-based decision-making across global futures markets. He is the creator of multiple trading methodologies, including the Sonic System, Atlas Line, and Trade Scalper, which help traders identify structured opportunities in markets such as the E-mini S&P 500 (ES), Nasdaq (NQ), crude oil (CL), and gold (GC). Official website: https://daytradetowin.com daytradetowin.com