Dumb Money’s Dive into Nvidia: A Close Call

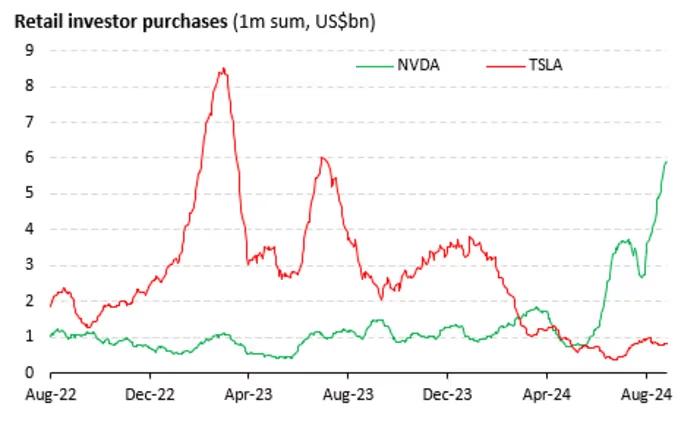

Retail investors, often labeled as “dumb money” on Wall Street, heavily invested in Nvidia before the company’s disappointing earnings announcement. Research from JPMorgan and Vanda shows that these individual investors not only bought Nvidia shares but also invested in exchange-traded funds (ETFs) heavily weighted with Nvidia, including leveraged ETFs tied to the company. NVDA -2.10% managed to beat analyst expectations in its quarterly report, both in earnings and sales, but issued cautious guidance that led to a 4% drop in its stock price, down to $120 in early premarket trading. The VanEck Semiconductor ETF SMH -1.68% , which has Nvidia as its top holding, dropped over 1%, while the GraniteShares 2x Long NVDA Daily ETF NVDL -4.26% and the Direxion Daily NVDA Bull 2X Shares NVDU -4.15% each fell 9%. Despite the market reaction, it wasn’t a total loss for retail investors. Many who bought Nvidia after its pullback in July still hold profitable positions. Vanda Research indicates that these investors have an average cost basis of $115, so most remain in the black even after the recent drop. This behavior contrasts with that of professional investors. Hedge funds had already reduced their stakes in Nvidia and other major tech stocks, the “Magnificent 7,” from their first-quarter highs, according to JPMorgan. Similarly, active equity mutual fund managers have been underweight in Nvidia. Vanda analysts compared this retail investment trend to the surge in Tesla TSLA -1.65% purchases before its 2023 annual general meeting. Following that meeting’s lackluster outcome, Tesla shares took two months to recover from the retail-driven spike before resuming their upward trend.