This year, the renowned 60:40 portfolio is outperforming last year’s performance, living up to expectations. This classic allocation, commonly favored by retirees and those nearing retirement, divides investments with 60% in stocks and 40% in bonds. While it faced a challenging year in 2022, experiencing one of its worst calendar-year losses in the history of U.S. markets, it has made a strong recovery in the current year.

The revival of this portfolio is not the result of intricate market-timing predictions but rather aligns with the concept of “regression to the mean,” often referred to as the “most powerful force in financial physics.” This concept suggests that following a period of extreme returns, the portfolio’s subsequent performance tends to gravitate back toward its long-term average.

Up until October 18, a portfolio structured with 60% invested in the Vanguard Total Stock Market Index ETF (VTI) and 40% in the Vanguard Long-Term Treasury Index Fund (VGLT) has demonstrated a year-to-date gain of 2.9%, which translates to an annualized gain of 3.8%. This starkly contrasts with the 23.5% loss experienced in the previous year.

The return to the mean follows historical patterns, where a 60:40 portfolio that is rebalanced annually has an average annualized return of 7.1%. This year’s annualized return of 3.8% aligns more closely with this long-term average when compared to the significant loss of the previous year.

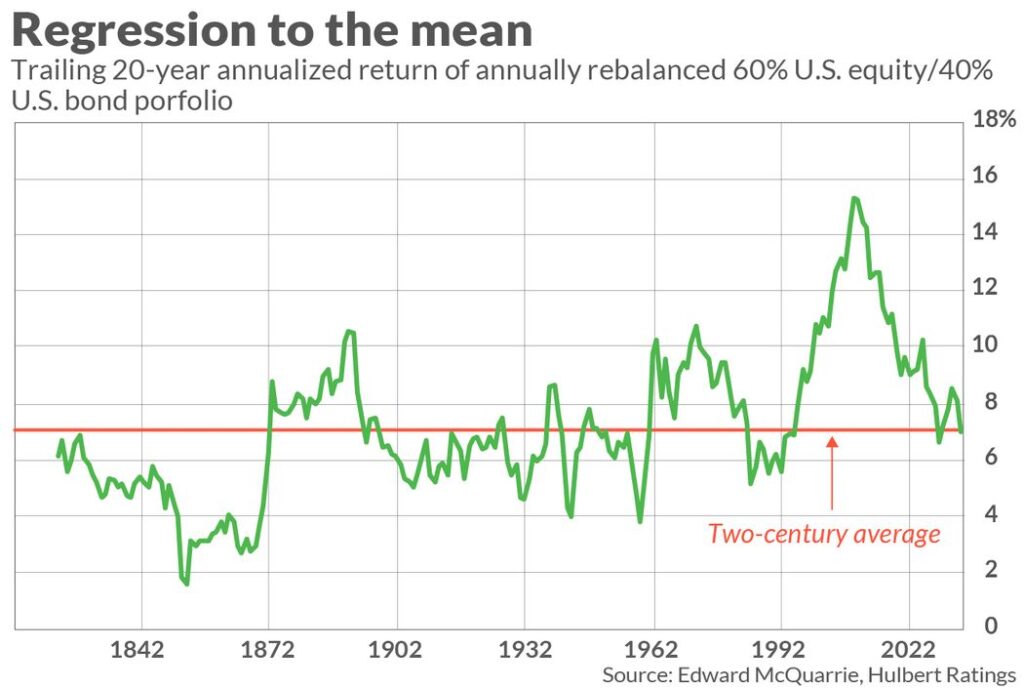

Illustrated in the accompanying chart is the 60:40 portfolio’s trailing 20-year return, which closely mirrors its long-term average. This evidence counters concerns from critics who argue that the portfolio is emerging from a period of unusually high returns, thereby implying expectations of lower future returns. This argument held weight 15 years ago when the trailing-20-year return was at a record high, but not today.

Reflecting on the past three years, when interest rates were at historic lows, it’s clear that many would have shied away from bonds and possibly reduced their equity exposure due to the widespread belief that rising interest rates negatively affect stocks. However, despite the rise in interest rates, the stock market has delivered a robust annualized three-year gain of 7.9%.

This equity return surpasses the performance of alternative asset classes that investors may have considered three years ago, such as gold bullion and hedge funds. In essence, the 60:40 portfolio would have kept investors invested in a superior-performing asset class.

While there are no guarantees in financial markets, it is a strong likelihood that the 60:40 portfolio will continue to perform well if interest rates significantly decline in the future. This is because a decrease in interest rates is traditionally seen as favorable for stocks, although historical evidence suggests that it does not always play out as expected. In the event of an unexpected downturn in the stock market, a 60:40 portfolio can help mitigate losses and potentially produce gains.

The 60:40 portfolio serves as a reliable insurance policy that frequently cushions the impact of an equity bear market. Three years ago, when interest rates were exceptionally low, this insurance component was minimal. However, with interest rates currently at a 16-year high, the bond portion of the 60:40 portfolio has significant potential to offset equity losses.

Typically, acquiring such insurance comes at a considerable cost, but over the past three years, the 60:40 portfolio not only provided protection but also generated returns. It’s as though investors have been paid to maintain this valuable insurance policy.

Disregarding the 60:40 portfolio at this stage would mean relinquishing this valuable insurance policy, which, in most scenarios, has proven to be a prudent choice.

John Paul is the founder of DayTradeToWin, a trading education and software company established in 2008, supporting traders worldwide. His expertise focuses on price action-based futures trading strategies and structured market analysis.

DayTradeToWin delivers trading education, indicators, and software tools designed to help traders apply disciplined, rule-based decision-making across global futures markets.

He is the creator of multiple trading methodologies, including the Sonic System, Atlas Line, and Trade Scalper, which help traders identify structured opportunities in markets such as the E-mini S&P 500 (ES), Nasdaq (NQ), crude oil (CL), and gold (GC).

Official website: https://daytradetowin.com