Trump’s Economic Agenda: Cutting Back on Stock Buybacks

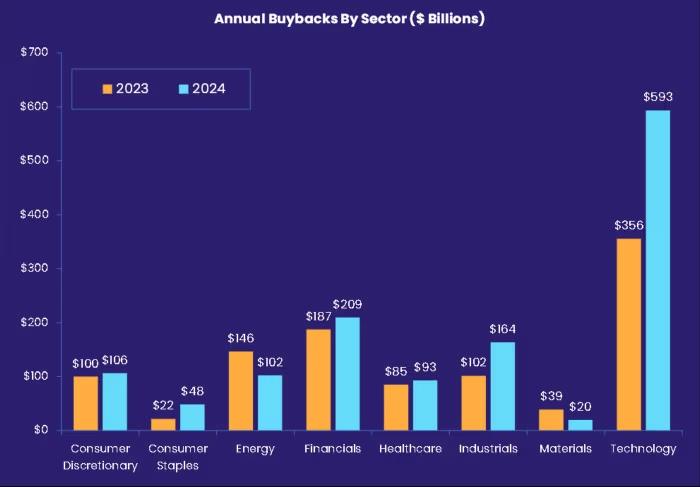

Tech Companies Ramp Up Stock Buybacks Despite Energy-Intensive Operations Tech companies have significantly increased their stock buybacks programs in recent years, prioritizing shareholder returns even as the industry’s energy demands continue to soar. Innovations like artificial intelligence (AI) and cloud computing require enormous amounts of energy to power data centers and support technological advancements, adding to the sector’s operational challenges. During Donald Trump’s second term, the administration’s “America First” policies focused on energy deregulation and revitalizing domestic industries. These priorities aimed to reduce costs and boost economic growth by leveraging abundant energy resources. However, experts from TS Lombard emphasized that achieving these goals would require U.S. companies to redirect more capital into infrastructure, equipment, and technology development rather than prioritizing stock buybacks and dividends. Steven Blitz, chief U.S. economist at TS Lombard, pointed out the dilemma: “Buybacks improve short-term returns on equity, which supports stock prices, but they divert funds from long-term investments crucial for growth.” In 2023, companies in the S&P 500 announced a record $1.34 trillion in buybacks, with nearly 70% of their internal funds going toward rewarding shareholders instead of reinvesting in growth-oriented initiatives. While tech firms have led buyback programs, they are also at the forefront of energy consumption due to their push to dominate AI and other high-demand technologies. Blitz noted that expanding energy infrastructure could indirectly benefit these companies by supporting the data-center growth necessary for the U.S. to maintain its leadership in emerging technologies. The challenge lies in finding a balance. While buybacks can enhance stock valuations in the short term, the tech sector’s reliance on energy underscores the importance of investing in sustainable infrastructure and innovation to secure long-term growth and competitiveness. John PaulJohn Paul is the founder of DayTradeToWin, a trading education and software company established in 2008, supporting traders worldwide. His expertise focuses on price action-based futures trading strategies and structured market analysis. DayTradeToWin delivers trading education, indicators, and software tools designed to help traders apply disciplined, rule-based decision-making across global futures markets. He is the creator of multiple trading methodologies, including the Sonic System, Atlas Line, and Trade Scalper, which help traders identify structured opportunities in markets such as the E-mini S&P 500 (ES), Nasdaq (NQ), crude oil (CL), and gold (GC). Official website: https://daytradetowin.com daytradetowin.com