U.S. Stock Market Overvaluation vs Non-U.S. Stocks: A Safer Bet?

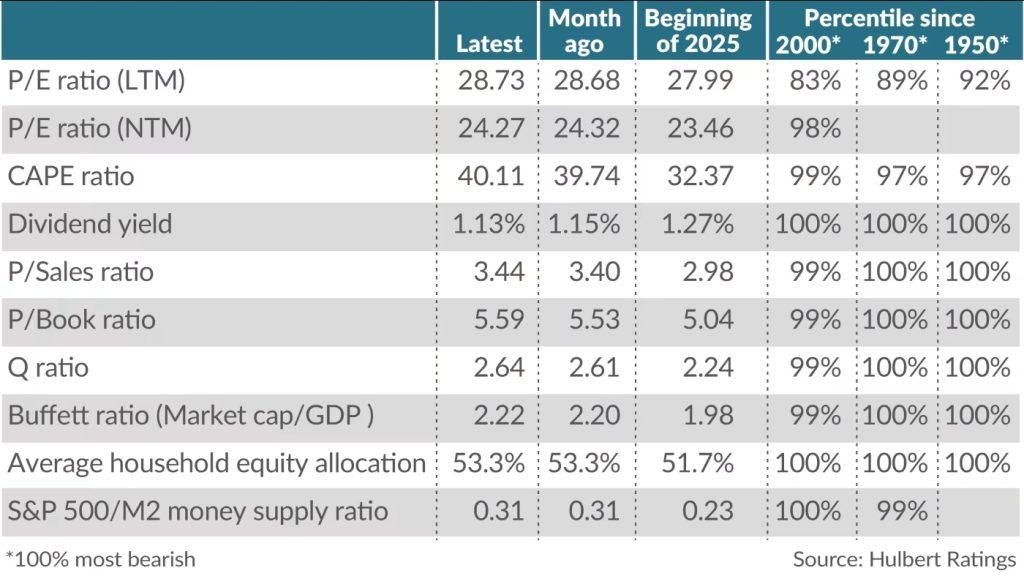

Valuation signals are flashing deep red for U.S. stocks, while non-U.S. markets appear far more attractive. It’s hard to imagine valuation indicators painting a more bearish picture for U.S. equities than they do today. By nearly every measure, U.S. stocks are priced at extreme levels. Meanwhile, non-U.S. stocks have already delivered more than twice the return of the S&P 500 this year, and there’s a compelling case that their strong performance will continue into 2026. For investors who want to stay invested in equities but are increasingly uneasy about lofty U.S. valuations, global markets offer a more appealing alternative. Many U.S. investors may not realize how strong non-U.S. performance has been in 2025, as headlines have been dominated by the “Magnificent Seven” and the AI-driven rally. Yet through Dec. 26, the S&P 500 is up 16.3%, while non-U.S. stocks have surged 33.1%, based on the MSCI All-Country World ex-U.S. index. A weaker U.S. dollar helped fuel some of that outperformance, boosting dollar-based returns for overseas assets. Even so, non-U.S. equities remain significantly cheaper than U.S. stocks after their rally. That valuation gap suggests non-U.S. markets could continue to outperform in 2026, even if the dollar stops falling. The contrast becomes even clearer when looking at cyclically adjusted CAPE ratios, which compare current market levels to the past 10 years of inflation-adjusted earnings. This valuation metric, popularized by economist Robert Shiller, highlights how stretched U.S. equities have become. According to Barclays Indices, the U.S. CAPE ratio is higher than those of roughly two dozen other global markets. On average, those countries trade at just over half the valuation of the U.S. Overvaluation warnings The CAPE ratio is just one of 10 valuation indicators tracked monthly for their ability to forecast long-term, inflation-adjusted returns. Today, all 10 point to the same conclusion: U.S. stocks are extremely overvalued. The latest readings place the average valuation percentile at 98%, meaning the market is more expensive than at nearly any other point in U.S. history. It’s difficult to envision a more cautionary signal. That leaves investors with a critical question: Will U.S. stocks once again defy gravity in 2026, or will far cheaper non-U.S. markets prove to be the safer — and stronger — bet?