Is the Dow Slide a Warning Sign?

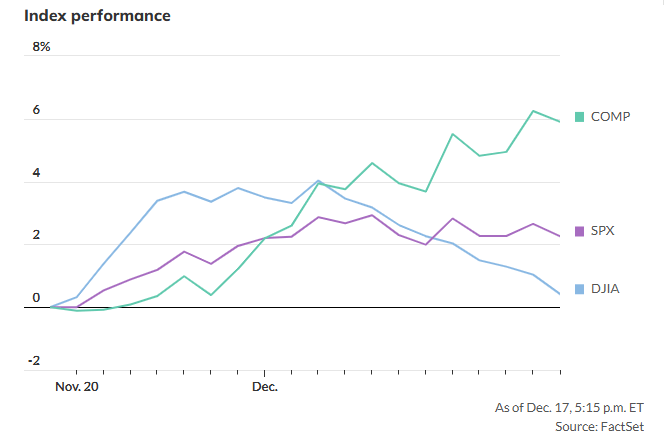

Factors Behind the Dow Slump The Dow Jones Industrial Average has fallen for nine consecutive days, marking its longest losing streak since 1978. This downturn has caught many investors off guard, particularly after the strong postelection rally that drove stocks to record highs. While the S&P 500 and Nasdaq Composite remain near their peak levels, the Dow has struggled. On Tuesday, it closed below its 50-day moving average for the first time since the November election, raising concerns about its underlying momentum. What’s Driving the Decline? Weak Market Breadth The Dow’s challenges reflect a broader trend across the market. Since early December, previously strong sectors have faltered, and investors have shifted back to Big Tech and semiconductor stocks like Broadcom Inc. In contrast, value-focused sectors such as small caps and financials have underperformed. Financials in the S&P 500 have dropped 4.4% this month, with utilities and energy performing even worse. While tech leaders have supported the S&P 500 and Nasdaq Composite, the Dow’s narrower composition has made it more vulnerable to sector-specific weakness. Market breadth has also been a concern. For 12 consecutive trading days, more S&P 500 stocks have declined than advanced, setting a record since at least 1999. Only 40.6% of S&P 500 stocks are currently trading above their 50-day moving averages, the lowest level since May. Individual Stock Pressures Much of the Dow’s recent losses can be attributed to one company: UnitedHealth Group Inc. Since the losing streak began, UnitedHealth has contributed 750 points to the Dow’s 1,564-point decline, accounting for nearly half of the drop. The company has faced pressure from congressional scrutiny over its pharmacy benefit manager business and negative headlines related to the death of a top executive. Other laggards dragging down the index include Sherwin-Williams Co., Caterpillar Inc., and Goldman Sachs Group Inc. Rising Treasury Yields Another factor weighing on the market is rising Treasury yields. The 10-year Treasury yield has climbed 20 basis points this month to 4.397%, fueled by concerns that the Federal Reserve may pause its interest rate cuts and that inflation could remain elevated. Higher yields have particularly impacted the equal-weighted S&P 500, which has significantly underperformed its market-cap-weighted counterpart this month. Outlook for Investors Despite the Dow’s recent struggles, there are reasons for optimism. The U.S. economy is on track to grow at over 3% in the third quarter, and corporate earnings forecasts for next year remain robust. According to Mona Mahajan, a senior investment strategist at Edward Jones, lagging sectors like small caps and value stocks may rebound due to their attractive valuations. However, a broader market recovery may depend on interest rates stabilizing and inflation remaining under control. As the Federal Reserve prepares to announce its next rate decision and economic projections, investors will be watching closely for signals about future policy moves and market direction.