Investor Panic: Iran-Israel Threats Trigger Rush to Safe-Haven Assets

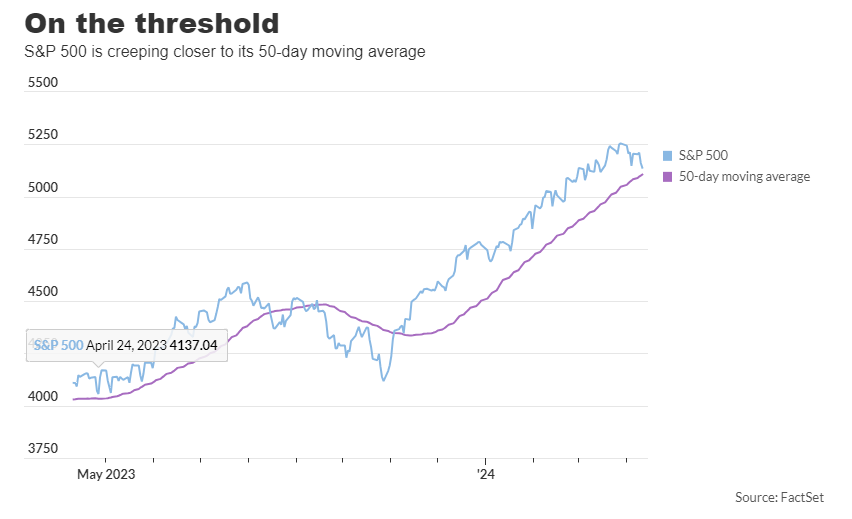

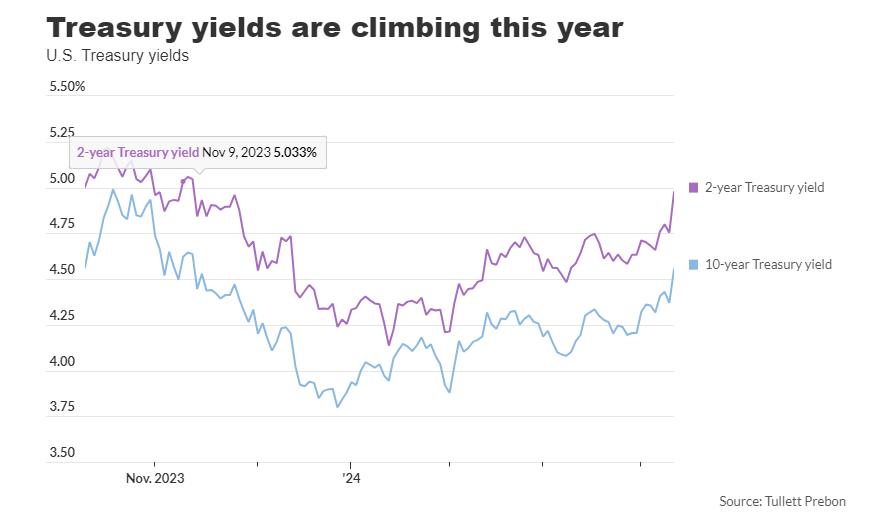

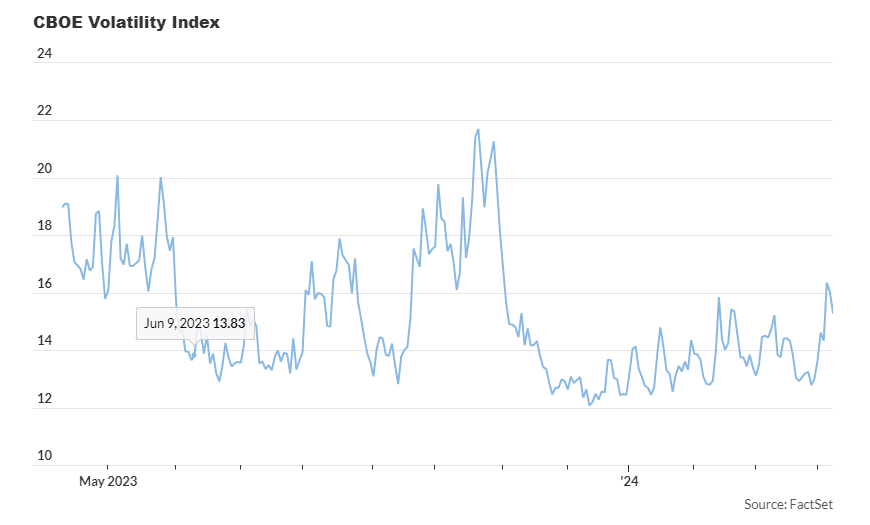

On Friday, Treasury bonds, gold, and the American currency all saw their worth rise, as investors sought out assets that could shelter them from potential losses in the stock market. The announcement of Israel’s readiness for a potential strike from Iran prompted investors to opt for safer investment options on Friday. As a result, they opted to sell stocks and instead put their money into Treasury bonds, gold, and the U.S. dollar. The start of the sell-off was triggered by a report in the Wall Street Journal that claimed Israel was getting ready for a potential attack from Iran, expected to happen by the end of the week. This reminded investors of a previous market drop on April 4, when stocks fell sharply following a similar warning from Israel. James St. Aubin suggests that the current state of affairs in Iran introduces a new dimension to the ongoing narrative. He posits that this is driving the market activity observed today. By noon in New York, the S&P 500 was on track for its biggest weekly drop since January, while the Nasdaq Composite had erased its earlier gains from the week when it hit a record high on Thursday. Simultaneously, the DJIA dropped nearly 500 points, leading to the blue-chip index experiencing its lengthiest string of losses since June and its biggest two-week percentage decrease since March 2023, according to Dow Jones Market Data. Market experts believed that the release of the report exacerbated the ongoing decrease in stock prices. They explained that investors were cautious about holding onto stocks over the weekend because they were worried about the possible consequences of Iran following through on its threats. Undoubtedly, the decline in the stock market this week can be linked to several reasons, such as an inflation report that exceeded expectations and investors’ tepid response to the earnings of prominent banks. The drop in stock prices led to a surge in demand for options to hedge against market volatility. This resulted in the Vix, also known as the fear gauge on Wall Street, spiking to its highest level since October 30, according to Dow Jones Market data. The index saw a more than 25% increase in recent trading sessions, marking its largest daily gain since November 2021. According to Tyler Richey, co-editor of Sevens Report Research, the increase in Vix resulted in a temporary situation where the price of Vix futures contracts expiring this month exceeded those expiring in May. This caused an inversion of the Vix futures curve for the first time since February. Richey pointed out that a Vix futures curve that slopes upward suggests that traders are getting ready for a continued decline in stock prices in the upcoming weeks. According to data from FactSet, investors also sought safety in bonds, leading to a drop in Treasury yields. The yield on the 10-year Treasury note decreased by 6 basis points to 4.51%. Even though Treasury yields have gone down, the U.S. dollar’s value has continued to rise, as shown by the ICE U.S. Dollar Index DXY increasing by 0.6% to 105.95. This marks its most successful week in 17 months. Analysts believe that the reason for this discrepancy between the dollar and yields is due to a safe investment strategy. The impact was also observed in the commodity markets, where gold futures reached historic highs. The main gold contract rose by $35.30, or 1.5%, hitting $2,407 per ounce. Furthermore, U.S.-traded West Texas Intermediate Crude futures increased by 1.5% to $86.23 per barrel, regaining much of the losses from earlier in the week. Rarely do geopolitical occurrences have such a profound impact on the stock exchange. Even declines stemming from major historical events, such as the September 11 attacks, typically bounce back within a short span of time. Market experts are of the opinion that the conflict in the Middle East will not significantly impact corporate earnings. Nevertheless, analysts at BofA Global Research have identified several potential negative implications for US multinational companies as a result of the conflict. A recent report discussed concerns regarding the potential effects on global trade and the European economy following the attack by Hamas on Israel on October 7th. The report highlighted worries about possible increases in energy prices, similar to those experienced after Russia’s invasion of Ukraine. Nevertheless, some investors warned that the decrease in stock prices on Friday might be temporary, just like the situation on April 4. Michael Lebowitz, a portfolio manager at RIA Advisors, proposed that the news of a possible attack from Iran was probably a strategic move in negotiations. He indicated that the drop in stock prices on Friday was more likely a result of the market being overpriced following a substantial five-month rise in value. In a recent interview with MarketWatch, Steve Sosnick, who is the chief market strategist at Interactive Brokers, mentioned that traders tend to get too excited when there is a rise in geopolitical tensions. Iran has reportedly issued a threat of retaliation against Israel after an Israeli airstrike on an Iranian embassy in Damascus, Syria led to the deaths of several important Iranian officials. John PaulJohn Paul is the founder of DayTradeToWin, a trading education and software company established in 2008, supporting traders worldwide. His expertise focuses on price action-based futures trading strategies and structured market analysis. DayTradeToWin delivers trading education, indicators, and software tools designed to help traders apply disciplined, rule-based decision-making across global futures markets. He is the creator of multiple trading methodologies, including the Sonic System, Atlas Line, and Trade Scalper, which help traders identify structured opportunities in markets such as the E-mini S&P 500 (ES), Nasdaq (NQ), crude oil (CL), and gold (GC). Official website: https://daytradetowin.com daytradetowin.com