The Dow Jones Industrial Average has lately recorded its ninth consecutive day of growth, marking its longest streak of consistent gains since 2017.

Interestingly, the latest advancements occurred in a session that also saw the Nasdaq Composite COMP drop by 2%. This marks its biggest fall in the past four months.

Could the broadening of marketplace activities be a sign of a sustained surge in the bull market? Or could the plummeting of technology stocks hint at a substantial fall for the S&P 500, which currently stands at an 18.1% growth this year? Worth noting is that even the ever-optimistic Tom Lee, Fundstrat’s Research Head, advises on cashing in some gains, describing it as “healthy”. Lee, in a recent report, claims that the uptick in suggestions for a considerable market retreat is due to recent instability. This unrest is marked by the underperformance of leading tech stocks and the rise in defensive sectors such as healthcare, utilities, and staples, together with negative responses from technical metrics. Consequently, he advises caution over a potential 5% market correction that could lead to a tumble of 200-225 points in the S&P 500; a development he predicts would stress investors.

Nonetheless, keeping in mind that this is Tom Lee, it’s important to be aware of the included warning – that any predicted decrease should be small. Here’s why.

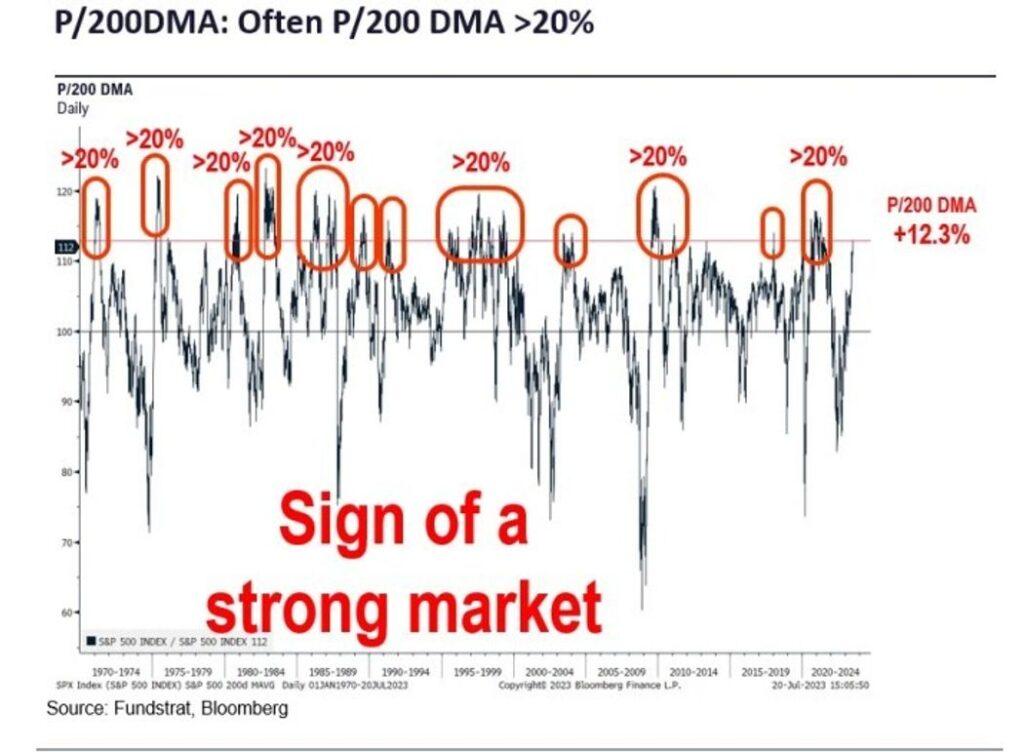

Firstly, the concerns that the market is expanding beyond its capacity are overblown. Some market participants are worried about the S&P 500 index surpassing its 200-day moving average by more than 12%, indicating over-buying. However, as shown in the subsequent graph, in eight of the past twelve instances where the market increased significantly above the trend line, it still ascended an additional 20% or more. According to Lee, this only signals a strong market.

Institutional investors are displaying indications of skepticism. Bank of America’s latest fund manager survey indicates that these entities have allocated the smallest portion to stocks in their asset category.

A new study by JPMorgan shows that only 17% of institutions intend to increase their stocks portfolio soon, a drastic decrease from 85% in January 2022. This negative outlook could serve as a valuable opposing indicator.

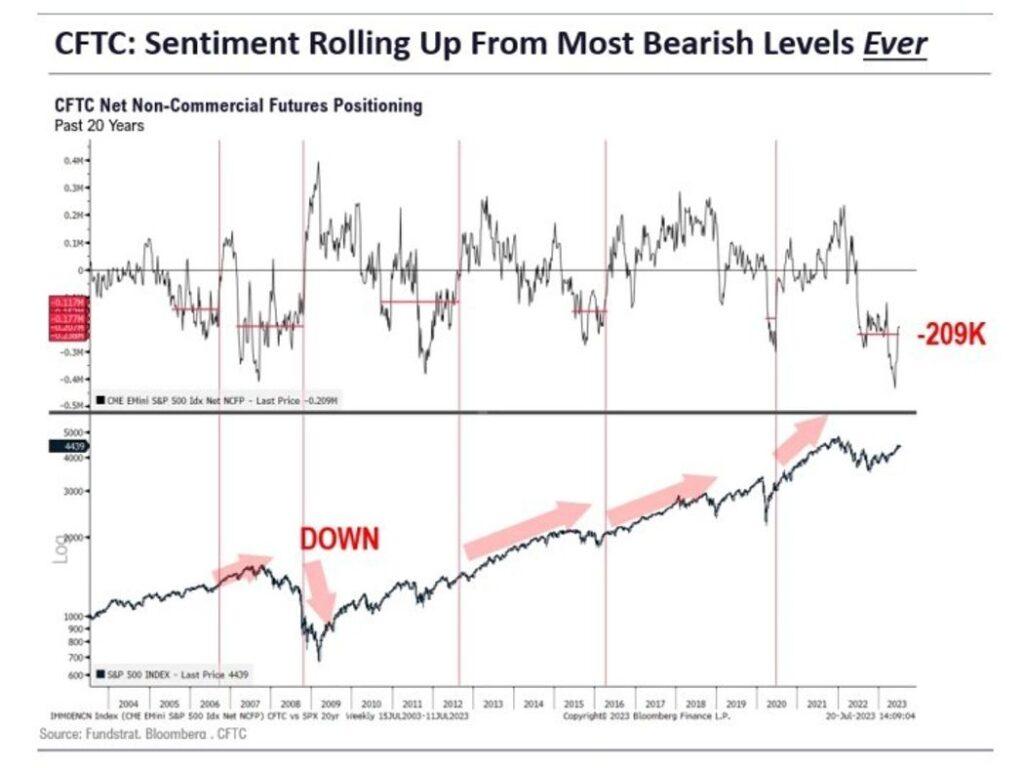

Furthermore, the traditionally negative positioning in S&P 500 futures has started to change, a trend that according to Lee, signaled “substantial upward movements” in stocks in four of the past five occurrences.

Lee is of the opinion that certain important events happening in the next few weeks can potentially lead to a decrease in interest rates, potentially boosting the stock market. For example, the policy decision of the Federal Reserve on July 26th might signal the last rise in rates for this cycle. A few days afterward, the data from the June PCE deflator should indicate the benign June CPI report. Moreover, the July CPI report, published on August 10th, could also demonstrate similar deflationary trends.

Lee concludes: “We are of the opinion that the next two to three weeks may bring positive influencing factors that could trigger an unanticipated beneficial reaction from the markets. Therefore, the timeframe for any market adjustment is somewhat limited. This suggests that the existing market downturn could potentially rebound by July 26th.”

John Paul is the founder of DayTradeToWin, a trading education and software company established in 2008, supporting traders worldwide. His expertise focuses on price action-based futures trading strategies and structured market analysis.

DayTradeToWin delivers trading education, indicators, and software tools designed to help traders apply disciplined, rule-based decision-making across global futures markets.

He is the creator of multiple trading methodologies, including the Sonic System, Atlas Line, and Trade Scalper, which help traders identify structured opportunities in markets such as the E-mini S&P 500 (ES), Nasdaq (NQ), crude oil (CL), and gold (GC).

Official website: https://daytradetowin.com