Optimism Amidst the S&P 500’s 30% Rally: Why Some Investors Believe the Market Isn’t Overextended

The S&P 500’s remarkable 30% rally since its mid-October low has caught the attention of investors, raising concerns about a possible correction due to the perceived stretch in the market.

However, Fundstrat’s Tom Lee offers a different perspective. In a Friday note, he acknowledges the potential for a typical 5% pullback but argues that such a decline could present a buyable dip, suggesting that the stock market might not be as overextended as some fear.

Lee points to upcoming catalysts that could bolster the stock market‘s bullish position. The Federal Reserve meeting on July 26 may mark the last rate hike of this cycle. Additionally, the release of personal consumption expenditures price data on July 28 is expected to reflect the cooling inflation trends observed in the June CPI report. Furthermore, the July CPI report, scheduled for August 10, is anticipated to show continued disinflationary pressures.

“We believe the next 2-3 weeks have positive fundamental catalysts that could pleasantly surprise the markets. This means the correction path has a somewhat narrow window. In other words, the weakness could reverse by July 26,” Lee stated. “Fundamental drivers keep us constructive, even with the S&P 500 appearing overbought.”

Apart from these fundamental catalysts, Lee presents three indicators suggesting the stock market isn’t excessively extended:

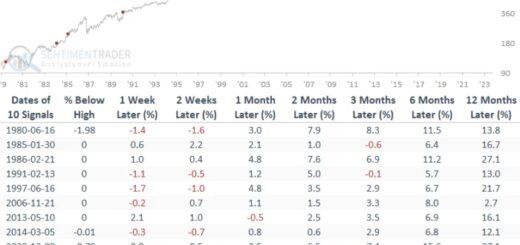

- S&P 500 vs. its 200-day moving average: Despite being 12% above its 200-day moving average, historical data reveals that the S&P 500 has traded more than 20% above this average at least eight times since 1970, indicating a robust market.

- Bearish sentiment among professionals: Institutional investors show a mere 17% inclination to increase equity exposure, marking a multiyear low. In contrast, back in January 2022, a substantial 85% planned to add more stocks to their portfolio. Moreover, Bank of America’s July fund manager survey indicates that equities rank as the most underweight asset class, with bonds holding the biggest overweight position. This skepticism among professionals suggests potential opportunities in the market.

- Retail sentiment in early stages of turning bullish: Although the AAII weekly investor sentiment survey shows that retail investors have become bullish amid the recent stock market rally, their sentiment is still in the early stages of bullishness. Lee notes that this shift in retail sentiment comes after an extended period of bearishness, implying the possibility of prolonged gains as investors gradually become more bullish.

Amid the looming concerns of a correction, these indicators and upcoming catalysts provide reasons for optimism regarding the stock market‘s resilience and potential for further gains.