Navigating the Shadows: Big Tech’s Dominance Echoes Dot-Com Bubble, Strategists Caution

A group of quantitative strategists from J.P. Morgan is drawing parallels between the ongoing stock-market surge, which has propelled the S&P 500 to six consecutive record closing highs in 2024, and the dotcom bubble.

Led by Khuram Chaudhry, the analysts highlight the increasing concentration in the U.S. stock market as a significant risk for investors in the current year. While acknowledging distinctions between the two periods, the team argues that the similarities are more notable than initially thought.

In a note disclosed by MarketWatch on Tuesday, Chaudhry and the team contend that historical context often downplays comparisons to the dotcom era, emphasizing the presence of numerous similarities.

The analysis coincides with the evident imbalance in stock-market returns, favoring the largest U.S.-traded companies, often referred to as “the Magnificent Seven,” which significantly influenced the S&P 500’s 24.2% gain in the previous year, according to FactSet. This trend has persisted into 2024, pushing market concentration close to its highest level since 2000.

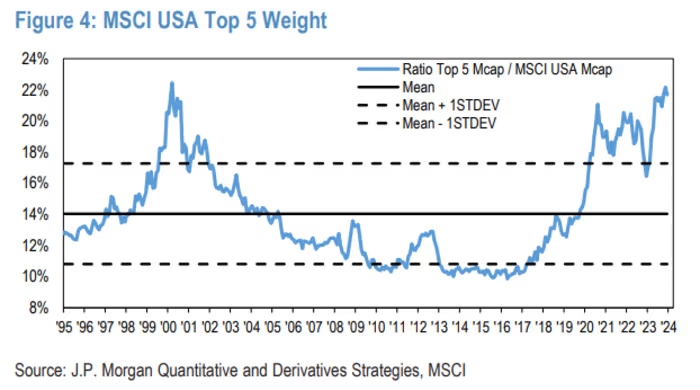

J.P. Morgan’s data reveals that the top five stocks constitute 21.7% of the MSCI USA Index as of the end of 2023, with the top 10, including the Magnificent Seven, accounting for 29.3%. This concentration is approaching levels seen in March 2000, just before the dotcom bubble burst.

Although the current top 10 are slightly below their historical peak share of 33.2%, recorded in June 2000, the concentration remains the highest since the dotcom era.

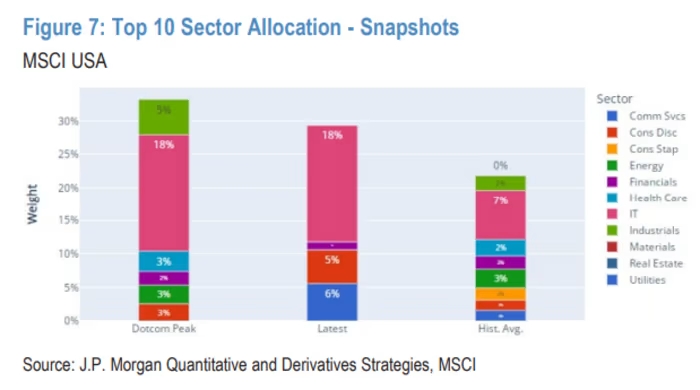

The analysis focuses on several factors, including the diversity of sectors represented among the top 10 most valuable companies. In 2024, only four sectors are represented, compared to six during the peak of the dotcom bubble. Information-technology companies, however, continue to dominate the group’s total market capitalization in both periods.

Despite differences in valuations, with today’s top 10 valued at 26.8 times forward earnings compared to the dotcom era’s peak of 41.2 times, the J.P. Morgan team emphasizes a crucial caveat. By considering the reciprocal of forward price-to-earnings, known as the forward earnings yield, they observe that as of October, the top 10 stocks commanded the highest premium to earnings relative to the rest of the index on record, though this premium has since diminished.

Furthermore, the team notes that the contribution of the 10 largest stocks to overall earnings per share (EPS) growth is smaller than during the dotcom days, challenging the notion of complete disconnection from fundamentals.

Lastly, the strategists anticipate a potential period of underperformance for Big Tech, suggesting that equity market drawdowns, possibly led by weakness in the top 10, may materialize. This cautionary stance is based on historical patterns of strong outperformance being followed by mean reversion.

As of Tuesday, most of the Magnificent Seven stocks were trading lower, contributing to a 0.7% drop in the Nasdaq Composite to 15,525, while the S&P 500 remained slightly off its most recent record closing high at 4,924.