Who Controls 10-Year Yields? The Market Has the Final Say, CIO Says

Federal Reserve Chair Jerome Powell may find some relief in the Trump administration’s latest focus on 10-year Treasury yields rather than pressuring the Fed for rate cuts. However, this shift in strategy has sparked fresh concerns among market participants.

Treasury Secretary Scott Bessent outlined the administration’s stance in interviews with Fox Business Network’s “Kudlow” program on Wednesday and Bloomberg Television on Thursday. Bessent emphasized that both he and Trump are concentrating on the 10-year Treasury yield (TMUBMUSD10Y 4.484%) rather than urging the Federal Reserve to cut interest rates. He also stated that the 10-year rate should decline “naturally” as a result of Trump’s economic policies.

While this reassured some that the administration would not interfere with the Fed’s independence—particularly after Trump’s January 23 demand for immediate rate cuts—others raised concerns about obstacles that could prevent lower yields. These include the inflationary impact of tariffs and the projected $2 trillion U.S. budget deficit for the 2024 fiscal year, which signals continued heavy Treasury issuance.

Mark Malek, Chief Investment Officer at New York-based wealth advisory firm Siebert, underscored a key point in an email: “Who is in control of 10-year yields? The answer is quite simple: THE MARKET. It is the market that has pushed 10-year yields higher recently. Bond vigilantes, if you will. These yields have risen due to expected inflation from trade frictions, increased deficit spending, and rising government debt.”

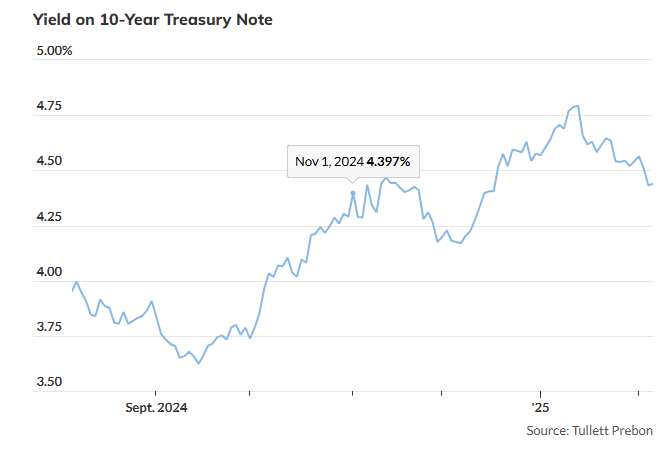

The 10-year Treasury yield, a key benchmark for borrowing costs—including mortgages, auto loans, and student loans—has surged more than a full percentage point, reaching 4.802% on January 13, up from 3.622% on September 16. On Thursday, it settled just below 4.44% after a week of declines following Trump’s announcement of new tariffs on Mexico and Canada and subsequent delays.

Malek acknowledged that the administration could theoretically drive yields lower by persuading the Fed to buy 10-year Treasury notes in the open market, a process known as yield-curve management. However, he considers such intervention unlikely. Historically, Japan employed yield-curve control until recently, targeting short-term rates near -0.1% and keeping its 10-year yield close to zero. Similarly, during and after World War II, the U.S. used yield-curve control from 1942 to 1951 to finance war debt.

Another potential strategy, Malek noted, would be for the Treasury Department to repurchase long-term Treasurys while issuing short-term debt, akin to the Fed’s 2012 Operation Twist program. However, such moves are complex and may have limited long-term effectiveness.

Despite Bessent’s comments, Thursday’s trading session showed a modest rise in Treasury yields across 2-year (TMUBMUSD02Y 4.275%), 10-year, and 30-year (TMUBMUSD30Y 4.692%) bonds, suggesting limited market reaction. Meanwhile, stock indices finished mixed, with the Dow Jones Industrial Average (-0.99%), S&P 500 (-0.95%), and Nasdaq Composite (-1.36%) posting declines.

Gregory Faranello, Head of U.S. Rates Trading and Strategy at AmeriVet Securities, acknowledged that targeting longer-term rates to lower borrowing costs is a “sound” approach but emphasized the need for precision in execution. “In a nutshell, it is hard to have your cake and eat it too,” he said, noting that bond yields typically decline when tariff policies are softened.

Faranello pointed out that with economic growth running above trend at 2% to 2.5% and inflation at 2.5% to 3%, there is limited room for rates to drop significantly. “If we can bring energy prices down, rates should follow on both the long and short ends,” he said. “That should be the real focus—energy prices, policy, and supply. But introducing other variables, like tariffs, complicates market interpretation.”

The sheer volume of government debt issuance each month also makes it difficult to sustain lower rates, he added. While an Operation Twist-style program remains a possibility, Faranello questioned its effectiveness. “I’m not convinced it makes a ton of sense given its limitations and the relatively minor long-term impact of such operations. The biggest driver of interest rates remains inflation.”

John Paul is the founder of DayTradeToWin, a trading education and software company established in 2008, supporting traders worldwide. His expertise focuses on price action-based futures trading strategies and structured market analysis.

DayTradeToWin delivers trading education, indicators, and software tools designed to help traders apply disciplined, rule-based decision-making across global futures markets.

He is the creator of multiple trading methodologies, including the Sonic System, Atlas Line, and Trade Scalper, which help traders identify structured opportunities in markets such as the E-mini S&P 500 (ES), Nasdaq (NQ), crude oil (CL), and gold (GC).

Official website: https://daytradetowin.com