Good News for Investors Amid Market Turmoil

With market volatility making headlines, discussing retirement optimism might feel out of place. Put Aside Your 401(k) Statement—These Retirement Trends Paint a Brighter Picture

However, David Stinnett, Vanguard’s head of strategic retirement consulting, remains hopeful. Despite inflation worries, federal job losses, and slow GDP growth, Stinnett points to positive shifts among retirement savers.

“You can have years of double-digit negative returns, high inflation, and unemployment — all of which we’ve seen recently — yet people are steadily improving their investing habits, participation rates, and savings contributions,” Stinnett said. “This week’s market fluctuations don’t worry me in the context of long-term savings.”

A Steady Climb Financial advisers often urge clients to stay the course during market downturns, and Vanguard’s early look at the 2024 “How America Saves” report backs up that advice. The report, which examines five million participants in Vanguard’s retirement plans, shows how American workers are building retirement savings consistently — and how the system is evolving to address key vulnerabilities.

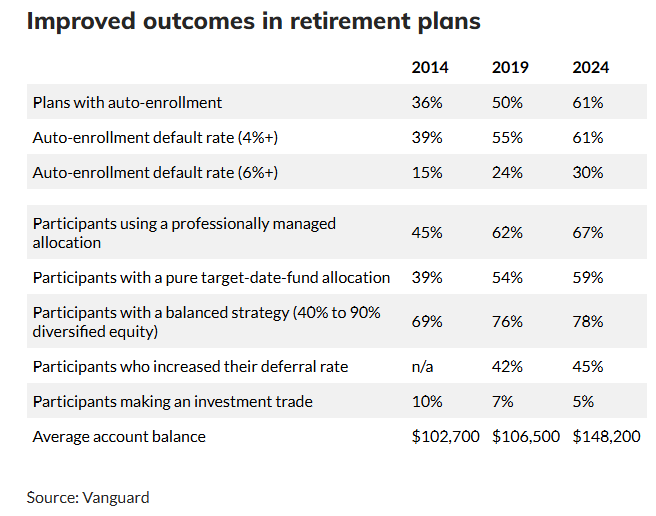

Auto-enrollment has been a game-changer. Ten years ago, just 36% of retirement plans had automatic enrollment. Today, that number has jumped to 61%, helping more lower-income workers start saving. Default contribution rates are also rising, with more companies enrolling workers at 4% and a growing number starting at 6%. Additionally, 45% of participants increased their savings rates in 2024.

Overcoming Roadblocks Despite these gains, many workers face setbacks. Job changes often reset contribution rates to lower default levels, slowing savings progress. “We need a smarter 401(k) system that ensures savings continue rather than restart,” Stinnett said.

Positive Balance Growth Average account balances climbed 10% in 2024 to $148,200, while median balances rose 8% to $38,176. However, hardship withdrawals also increased. Only 5% of participants took such withdrawals, which Stinnett attributed to regulatory changes and greater participation by lower-income workers. While the trend warrants attention, Stinnett does not see it threatening overall retirement readiness.

A Brighter Future Despite short-term economic uncertainty, Stinnett remains optimistic. “Our voluntary retirement system differs from the global norm, and employers, policymakers, and record keepers are continuously adopting best practices. These improvements are gradual but steady — in both good and bad years. That’s a message worth sharing.”

By focusing on consistent contributions and long-term strategies, American workers are proving that even in turbulent times, retirement goals can stay on track.