3 Red Flags as Stocks Near Bull Market

Stocks Are Booming — But Bonds, the Dollar, and Gold Tell a Different Story

The S&P 500 is flirting with bull market territory, ending Monday just shy of the 20% gain mark from its April low. Investors appear to have shrugged off Moody’s recent U.S. credit downgrade, pushing equities higher in what looks like a broad risk-on rally.

But beneath the surface, not all is well.

JPMorgan CEO Jamie Dimon warned Monday of “an extraordinary amount of complacency” in markets, and Lisa Shalett, Chief Investment Officer at Morgan Stanley Wealth Management, agrees. In a note to clients, she highlighted three major market signals that are diverging sharply from the bullish sentiment in stocks — and could spell trouble ahead.

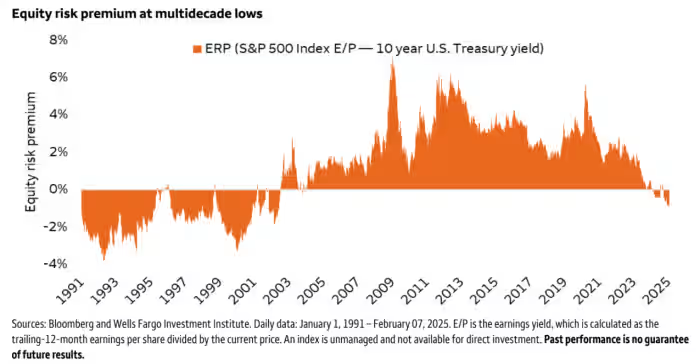

1. Treasury Yields Are Flashing Caution

While short-term Treasury yields reflect growing confidence in the economy, longer-term yields tell a more complex story. The 10-year yield is inching toward 4.5%, a level that reflects not just growth optimism, but also concern over rising real rates and growing U.S. debt burdens.

With Congress considering new tax, spending, and budget packages that could add $2 trillion in debt, Shalett warns this could drive interest costs sharply higher over the next decade. That means structurally higher rates — and lower valuations for stocks.

2. The Dollar’s Weakness Defies the Rally

Since peaking in January, the U.S. dollar has fallen 8% against major currencies, despite the surge in equities. Even more puzzling: the dollar is now moving with oil prices, reversing a long-standing inverse relationship.

Shalett suggests this signals a shift in global capital flows and reserve allocations. A weaker dollar could lead to diminished foreign investment in U.S. assets — another potential headwind for equities.

3. Gold Is Outperforming — and That’s Unusual

Gold, typically a hedge against turmoil, has been outperforming U.S. stocks since 2022. That’s not typical during a stock market boom. Shalett sees this as another sign that global investors — including central banks — are seeking alternatives to dollar-denominated assets.

“Strength in gold, disconnected from traditional safe-haven behavior, hints at structural shifts in global reserves and risk perceptions,” she said.

Not the Time for Complacency

Investors hoping for a repeat of the “Goldilocks” environment of 2023–2024 — falling real rates and a resilient dollar — may be in for disappointment. Shalett forecasts more modest average returns for U.S. equities (5%–10%) amid increased volatility, tighter financial conditions, and a weaker dollar.

Her advice: use the current rally to rebalance. She recommends increasing exposure to international equities, commodities, energy infrastructure, hedge funds, and shorter-duration investment-grade and municipal bonds.

“This is not the time to rely on valuation expansion,” she warned.