Inflation Recedes, Wall Street Revels in Continued Success Throughout the Week

Wall Street’s winning streak persisted for the fourth day on Thursday, following signs that inflation is progressively becoming less of a burden on the economy.

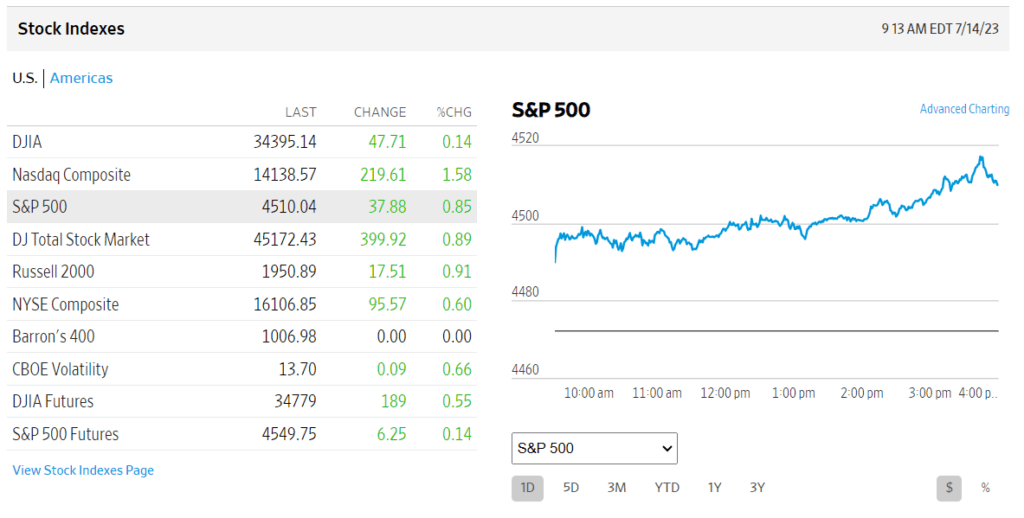

The S&P 500 increased by 0.8%, gaining 37.88 points and reaching 4,510.04 – its highest closing value since April 2022. The Dow Jones Industrial Average had a smaller increase of 0.1%, closing at 34,395.14 after gaining 47.71 points. The Nasdaq composite had a notable surge of 1.6%, rising by 219.61 points and reaching 14,138.57, driven by the strong performance of Big Tech stocks.

The S&P 500 is on track to experience its seventh week of increases in the past nine weeks. This is because recent data indicate that the rate of inflation is declining. As a result, there is optimism that the Federal Reserve will soon cease its efforts to raise interest rates. In June, there was lower-than-expected inflation in the wholesale sector, with producers paying only a 0.1% increase compared to the previous year. This is a significant drop from the 11.2% inflation recorded last summer.

Investors are worried about a possible economic downturn because of the notable inflation levels. To control prices, the Federal Reserve has raised interest rates, which has caused this concern. The increased rates hinder inflation by slowing the entire economy and affecting investment prices unfavorably. Furthermore, they can cause unexpected disruptions in specific sectors of the economy.

Traders strongly believe that the Federal Reserve will raise the federal funds rate in the next two weeks, the highest since 2001. Nevertheless, analysis of recent inflation data has caused traders to ponder if this might be the final increase in the current cycle.

A recently published report on Wednesday highlighted that consumer prices in June witnessed a 3% increase compared to the previous year. This demonstrates a substantial decline from last summer when the inflation rate was over 9%. Deutsche Bank economists aptly describe this as a “refreshing summer breeze.”

The decrease in traders’ predictions for future interest rate hikes by the Federal Reserve caused Treasury yields to keep dropping in the bond market.

The interest rate for mortgages and other important loans is affected by the 10-year Treasury yield, which dropped from 3.86% on Wednesday to 3.98% on Tuesday and is currently at 3.76%.

The interest rate on the two-year Treasury notes declined from 4.75% on Wednesday and 4.89% on Tuesday to 4.63%. This rate often changes in response to forecasts about the Federal Reserve’s future actions.

The rate of decline in yields accelerated when James Bullard revealed in the afternoon his intention to step down as the president of the St. Louis Federal Reserve Bank and take on the position of dean at Purdue University’s business school in the upcoming month. Bullard was recognized for advocating for higher interest rates to control inflation.

Lower interest rates positively impact different types of investments. However, many investors believe that technology and other stocks with high growth potential will yield substantial profits.

The S&P 500 experienced a boost due to the significant contribution of Amazon, Alphabet, and Nvidia. Amazon witnessed a growth of 2.7% as it announced that its annual Prime Day event had surpassed previous records and became its most profitable sales day ever.

After Google announced that they would be extending the availability of Bard, their artificial intelligence-powered chatbot, to various countries around the world and introducing more features, the stock of Alphabet witnessed a 4.7% increase.

Nvidia, a prominent presence in the field of AI and a company that has been generating buzz on Wall Street, saw a rise of 4.7%.

After exceeding analysts’ projections for profits in the spring, PepsiCo experienced a 2.4% increase in its stock value. Despite declining demand for beverages and snacks, the company achieved higher earnings by implementing price hikes. Furthermore, PepsiCo has revised its annual forecasts, expecting better results for the year.

Earnings reporting season has just started, and JPMorgan Chase will be the first bank to announce their profits for the spring period on Friday. Unfortunately, the overall forecast is not positive, with experts predicting a notable decrease in earnings for S&P 500 companies. This decline is expected to be the largest since the global economy was heavily affected by the pandemic last year.

Even though there is a risk of a recession, the job market has shown its ability to withstand it and has supported the economy. Recent statistics revealed fewer individuals filed for unemployment benefits last week than expected. However, it is important to acknowledge that an extremely strong job market might result in the Federal Reserve implementing more aggressive actions regarding interest rates and controlling inflation.

Chun Wang, a senior research analyst, and co-portfolio manager at Leuthold, has raised a concern that while inflation is showing some positive indications, there is a danger that Wall Street is quickly assuming it will decrease significantly, leading the Federal Reserve to lower interest rates and prevent a recession.

Wang’s report highlights a worry that the market is not giving enough consideration to the likelihood of inflation staying between 3% and 4% over the next six to 12 months. Wang suggests that the predictability of both inflation and the Federal Reserve’s policy is uncertain, as there is a suspicion that the widely held belief of a seamless economic transition will face significant challenges soon.

On Thursday, there was a decrease in Exxon Mobil’s stock market performance. The company’s stocks dropped by 1.8% after they announced their acquisition of Denbury, a company with pipelines for carbon dioxide. This acquisition, which is worth $4.9 billion in stock, caused Denbury’s stocks to also decrease by 1.3%.