Stocks have surged to unprecedented heights, prompting a reassessment of S&P 500 targets by Wall Street. However, exercising caution and resisting the allure of hype is prudent.

At the onset of the week, several strategists recalibrated their S&P 500 projections. Citigroup adjusted its mid-2024 estimate from 4400 to 5000, while Piper Sandler raised theirs from 4625 to 4825.

Even Mike Wilson of Morgan Stanley, who had previously predicted a significant 18% downturn, acknowledged the potential for a sustained market rally in a recent communication.

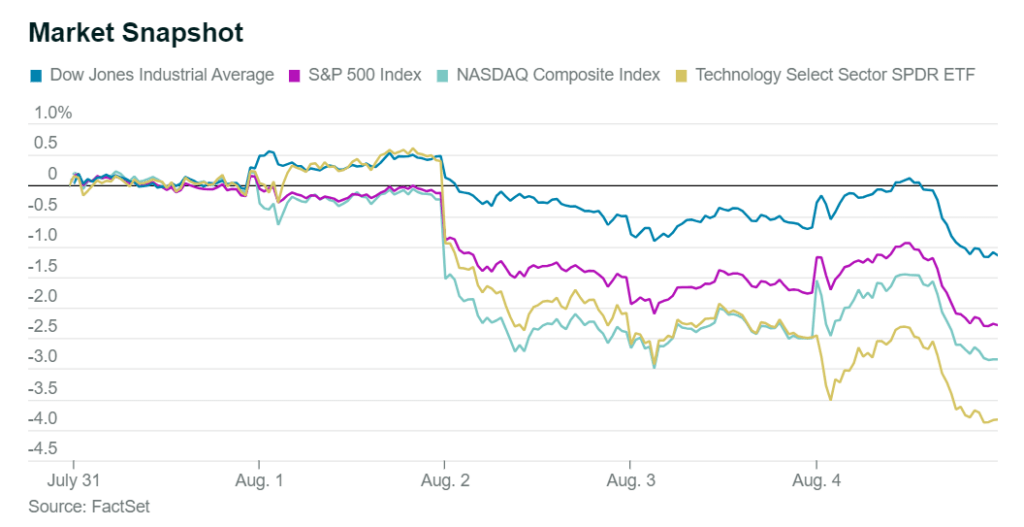

Interestingly, the week posed challenges for the stock market. The S&P 500 experienced a dip of 2.3%, the Dow Jones Industrial Average declined by 1.1%, and the Nasdaq Composite slid by 2.8%. Notably, the S&P 500 had already surged by 28% from its low during the bear market in October. The sheer magnitude of this rapid upswing caught strategists off-guard, prompting them to adjust their forecasts to align with the current market dynamics.

This adjustment is justified by recent events highlighting the economy’s resilience, even though it hasn’t reached a level that would compel unexpected actions from the Federal Reserve. The latest payroll report indicated a modest addition of 187,000 jobs in July and downward revisions for previous months. This suggests the possibility of a controlled deceleration.

Earnings have outperformed predictions as well, with Amazon.com (AMZN) notably standing out with an 8.3% gain after its report. This accomplishment is particularly noteworthy considering the premium valuation of the S&P 500.

Nevertheless, rushing to invest immediately after the S&P 500 achieved its strongest performance in the first seven months of a year since 1997 may be premature. The index remains relatively expensive, trading at over 19 times forward earnings for the next 12 months, up from approximately 15 times at the beginning of the rally. Moreover, certain stocks like Apple (AAPL), which played a pivotal role in the rally, exhibit signs of potential stagnation. This eagerness to invest appears to be driven by a sense of urgency and the fear of missing out.

Michael Arone, Chief Investment Strategist at State Street Global Advisors, observes the emergence of “FOMO” (fear of missing out) as even bearish investors seem to be capitulating. This sentiment heightens his concern, as it could potentially lead to a market downturn.

History validates Arone’s caution, not solely due to the typical summer market weakness. A comparison of the average S&P 500 target against the actual index reveals that Wall Street’s projections serve as coincidental indicators at best and lagging ones at worst. For instance, in 2022, these forecasts peaked shortly after the market reached its zenith in January.

In the recent week, a surge in Treasury yields triggered the market’s retreat. While the exact catalyst remains uncertain, it could be attributed to a combination of increased Treasury debt issuance, alongside robust economic data prompting a reevaluation of growth projections. Elevated yields diminish stock valuations, assuming other variables remain constant. Yet, if the rise remains moderate, it could present a buying opportunity.

This perspective gains further importance as the market sets its sights on 2024. According to Wells Fargo, a notable 61 S&P 500 companies that reported second-quarter earnings raised their profit guidance, while 23 lowered their outlooks. This contributes to analysts’ expectations of sales and earnings growth in the upcoming year.

In essence, the market’s attention is fixed on 2024, as Doug Bycoff, Chief Investment Officer of the Bycoff Group emphasized. He suggests a 5% pullback could be an advantageous entry point.

In conclusion, the pivotal lesson is not to hastily invest during periods of exuberance but to seize the opportunities presented by market downturns.

John Paul is the founder of DayTradeToWin, a trading education and software company established in 2008, supporting traders worldwide. His expertise focuses on price action-based futures trading strategies and structured market analysis.

DayTradeToWin delivers trading education, indicators, and software tools designed to help traders apply disciplined, rule-based decision-making across global futures markets.

He is the creator of multiple trading methodologies, including the Sonic System, Atlas Line, and Trade Scalper, which help traders identify structured opportunities in markets such as the E-mini S&P 500 (ES), Nasdaq (NQ), crude oil (CL), and gold (GC).

Official website: https://daytradetowin.com