Five percent is a relatively typical interest rate,” notes Michael Rosen, CIO at Angeles Investments. Throughout the year, consumer spending has defied expectations on Wall Street, maintaining stocks at near-record levels and preventing the U.S. economy from plunging into recession.

This coming week, sentiment surrounding stocks may pivot on two closely linked economic indicators: the consumer price index (CPI) for August, set to be released on Wednesday, and monthly U.S. retail sales data scheduled for the day after.

Jason Blackwell, chief investment strategist at The Colony Group, remarks, “They are holding on much longer than we all anticipated last year,” referring to consumers’ willingness to spend despite credit card interest rates exceeding 20% and inflation remaining above the Fed’s 2% annual target rate.

Blackwell remains optimistic about the consumer’s health and their ability to cope with rising prices. Last month’s yearly CPI reached 3.2%, down from last year’s peak of 9.1%. However, Blackwell will closely watch Wednesday’s economic update for any signs of relief in shelter costs, a persistent form of inflation that remained at 7.7% yearly in July, even as home prices decreased.

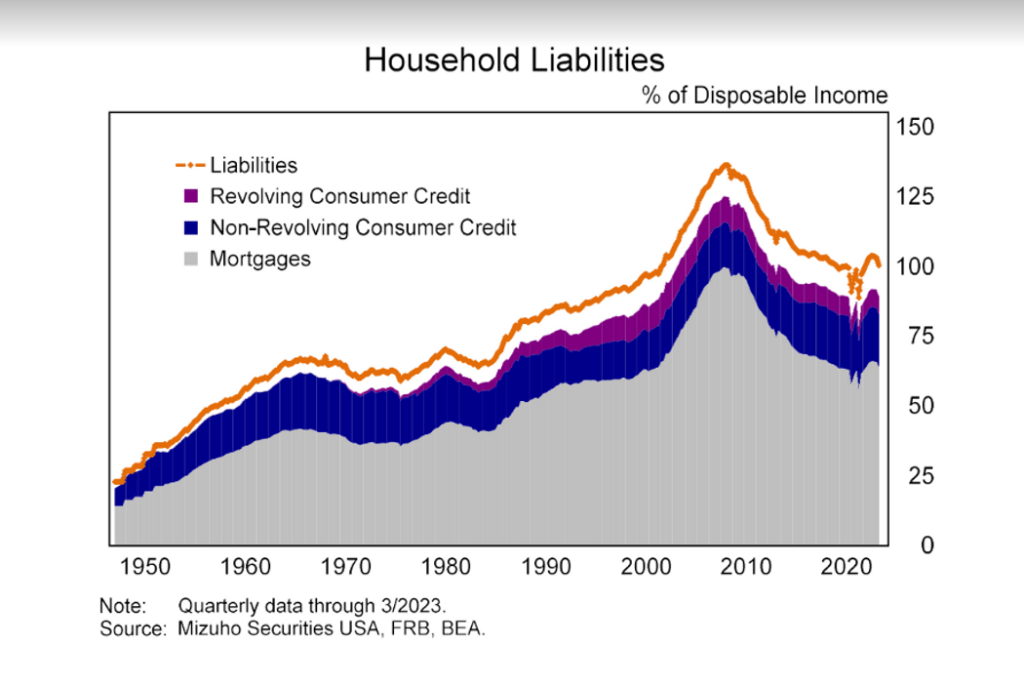

The surge in mortgage rates has had less impact on the housing market, thanks to homeowners having already refinanced at historically low pandemic rates. A decade of limited construction has also prevented prices from plummeting, leaving many homeowners with substantial home equity cushions. Coupled with rising wages and the economy’s resilience, these factors suggest a continued trend of spending, especially as household debt-to-income ratios remain near a 20-year low of about 100%, according to Mizuho Securities.

Michael Rosen, CIO at Angeles Investments, highlights that the market’s expectation of a recession has been consistently wrong over the past year. He believes that higher interest rates today are less concerning than some may think, especially given wage growth and strong household balance sheets, which can sustain economic activity, even as pandemic savings are depleted.

Rosen emphasizes the importance of the consumer sector, which dominates the U.S. economy, and notes that recent economic data and signs of activity, such as crowded airports, restaurants, and sold-out concerts by artists like Beyoncé and Taylor Swift, reflect this strength.

July saw the largest increase in sales at U.S. retailers in six months. While higher energy prices could affect August’s economic data, Rosen maintains a positive outlook for stocks and short-term Treasury securities.

He explains that markets often thrive amidst uncertainty and anticipates further stock market gains, emphasizing the influence of strong corporate profits.

John Butters, FactSet’s senior earnings analyst, predicts a net profit margin of 11.7% for the S&P 500 index in the third quarter, surpassing the 11.6% from the previous quarter and the five-year average of 11.4%.

Rosen reminds investors of the past, pointing out that interest rates reached double digits in the 1980s but remained high as the economy expanded. He considers a 5% interest rate to be relatively normal and even suggests that zero interest rates can be detrimental to the economy.

U.S. stock markets closed the week with losses: the S&P 500 index was down 1.3%, the Dow Jones Industrial Average fell 0.8%, and the Nasdaq Composite Index dropped 1.9%, according to Dow Jones Market Data. Nevertheless, the Dow remained only 6% away from its record high set in January 2022, and the S&P 500 was 7% below its prior peak. Yields on 3-month and 6-month Treasurys have remained above 5% since spring.

John Paul is the founder of DayTradeToWin, a trading education and software company established in 2008, supporting traders worldwide. His expertise focuses on price action-based futures trading strategies and structured market analysis.

DayTradeToWin delivers trading education, indicators, and software tools designed to help traders apply disciplined, rule-based decision-making across global futures markets.

He is the creator of multiple trading methodologies, including the Sonic System, Atlas Line, and Trade Scalper, which help traders identify structured opportunities in markets such as the E-mini S&P 500 (ES), Nasdaq (NQ), crude oil (CL), and gold (GC).

Official website: https://daytradetowin.com