S&P 500 Futures and Bonds Rally in Sync, Four-Month Highs on the Horizon

Rising confidence in the Federal Reserve’s inclination to implement interest rate cuts in the upcoming year shaped market sentiment.

Current Status of Stock-Index Futures:

- S&P 500 futures saw a 15-point uptick, representing a 0.3% increase, reaching 4578.

- Dow Jones Industrial Average futures contributed 105 points, or 0.3%, totaling 35550.

- Nasdaq 100 futures ascended by 61 points, or 0.4%, reaching 16109.

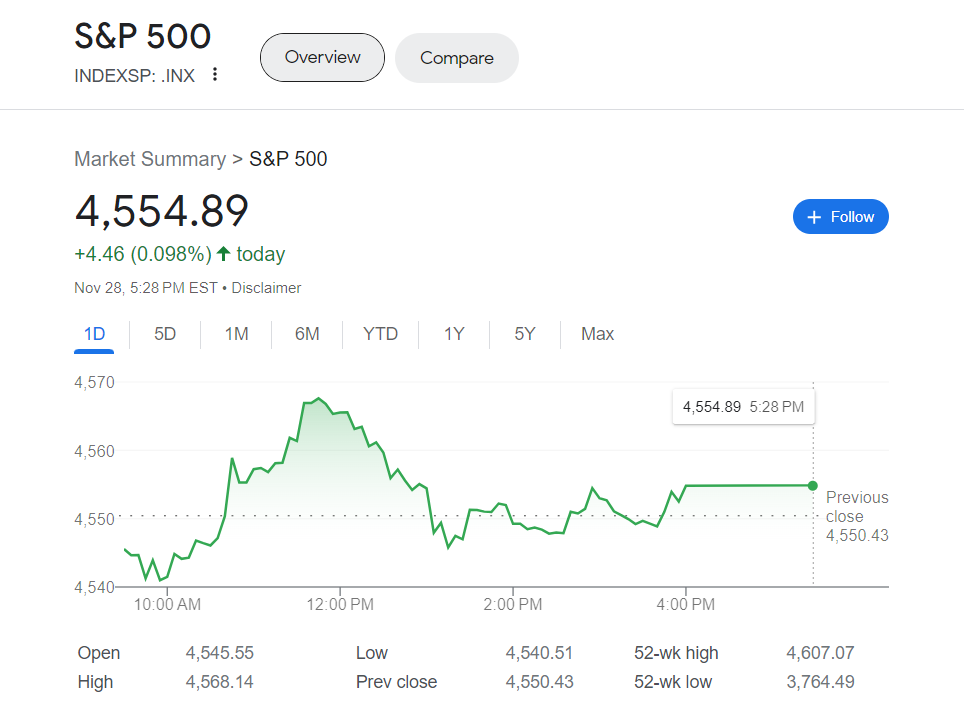

On Tuesday, the Dow Jones Industrial Average surged by 84 points (0.24%) to 35417, the S&P 500 advanced by 4 points (0.1%) to 4555, and the Nasdaq Composite gained 41 points (0.29%) to 14282.

Market Catalysts:

Index futures hinted at the S&P 500 preparing to commence Wednesday’s session challenging its peak levels since August, propelled by the continuous decrease in U.S. borrowing costs.

The 10-year Treasury yield, which surpassed 5% in October, dipped to approximately 4.25% in early trading. Investor confidence in the Federal Reserve initiating rate reductions in the coming months grew as concerns about inflation eased. The likelihood of a rate cut in March, by a minimum of 25 basis points, surged to 42%, up from 21% on Tuesday, according to the CME FedWatch tool.

Remarks from Fed Governor Chris Waller on Tuesday, indicating that existing policies are well-suited to guide the economy and control inflation, affirmed the market’s belief that the Federal Reserve is pausing interest rate hikes. This resonates with the prevalent market sentiment, where additional hikes had already been largely factored out earlier in the month, as highlighted by Stephen Innes, managing partner at SPI Asset Management.

Investor attention turns to Fed Chair Jerome Powell’s remarks on Friday to discern if they echo Waller’s ostensibly more dovish stance. On Wednesday, scheduled speeches from Fed officials, including Richmond Fed President Thomas Barkin and Cleveland Fed President Loretta Mester, add to market scrutiny.

On Wednesday, U.S. economic updates include the first revision of third-quarter GDP and the October trade balance in goods at 8:30 a.m. Eastern. The Federal Reserve’s Beige Book of economic anecdotes will be released at 2 p.m. Additionally, crucial inflation data, in the form of the PCE index for October, is set for Thursday.

The decrease in U.S. bond yields is impacting the dollar adversely, potentially offering additional support to U.S. corporations with international sales. The dollar index is at its lowest point since August, contributing to the rise in gold prices, now exceeding the $2,000 per ounce mark.

Despite the positive outlook, some observers express concerns about the recent optimism in the bond market, suggesting potential vulnerability not only in the S&P 500 but also in various market segments. Ipek Ozkardeskaya, senior analyst at Swissquote Bank, highlights overbought conditions across multiple asset classes, including U.S. bonds, the dollar, gold, and major currencies, hinting at the possibility of an impending correction.

Wednesday’s corporate earnings reports feature Foot Locker, Dollar Tree, and Petco Health and Wellness before the opening bell, followed by Snowflake, Salesforce, and Okta after the close.