Act Fast: Short the Dollar, Says Goldman Sachs

Happy CPI day to all who observe! Here’s a deeper look into today’s crucial report.

If inflation aligns with economists’ expectations, there could be a brief opportunity to bet against the U.S. dollar, according to Karen Reichgott Fishman, senior currency strategist at Goldman Sachs.

After reaching 2023 highs, the dollar has been declining and might weaken further. Fishman explains, “The tactical backdrop looks increasingly friendly for risk and negative for the dollar.”

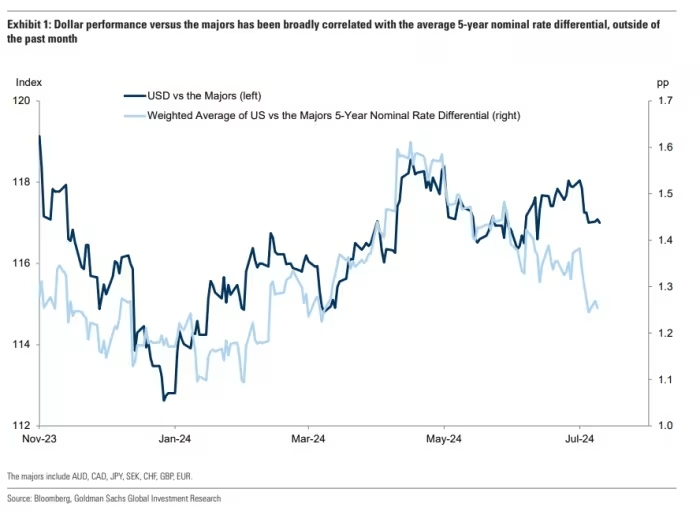

This year’s dollar fluctuations have primarily been driven by interest rate expectations, shown in a chart that plots the dollar against a weighted average of the rate differential in 5-year securities of major counterparts.

Comparing the dollar’s performance against major rivals reveals this trend: it has risen sharply against the Japanese yen (USDJPY), where rate differentials have widened, and fallen against the British pound (GBPUSD), with minimal changes.

Interest rates are not the only factor behind the dollar’s strength. Fishman notes that the second-largest contributor to the dollar’s gains has been the Mexican peso (USDMXN), influenced by a significant shift after Mexico’s landslide election.

Fishman also points out that the correlation between stocks and bonds has been mostly positive this year, which often coincides with broad dollar swings. When stocks and bonds rise together, the dollar typically struggles. “This makes it all the more surprising to see the dollar simultaneously hit new highs and reinforces the scope for a tactical sell-off,” she adds.

Currently, there appears to be a narrow window for further relief in U.S. yields and gains for U.S. equities, with few major obstacles expected until mega-cap tech earnings at the end of July. In such an environment, the dollar usually weakens against most currencies and becomes a good candidate for funding emerging-market carry trades.

However, Fishman emphasizes that the dollar’s bullish trend is likely to resume in the second half. Ahead of the U.S. election, broader tariffs, especially against the Chinese yuan and other Asian currencies, pose an upside risk. This is in addition to the expected limited cross-border investment flows leading up to the election.