The Central Bank Stealing the Fed’s Spotlight

This week, three of the world’s most influential central banks will reveal their monetary policy updates within about 32 hours.

On Thursday, the Bank of England might reduce borrowing costs, while the Federal Reserve is expected to hold rates steady on Wednesday but may hint at a potential rate cut in September.

The most critical decision, however, may come from the Bank of Japan (BOJ). Recently, a stock market downturn, particularly in large technology stocks, coincided with a rally in the Japanese yen.

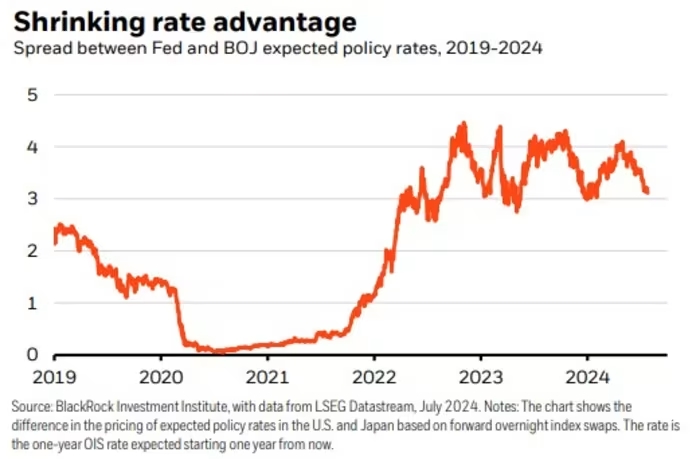

A theory emerged suggesting that if the BOJ raises interest rates and the Fed cuts rates (following recent soft inflation data), the yield gap between the U.S. and Japan would narrow, making the yen more attractive. Investors who had borrowed yen to buy U.S. mega-cap stocks had to reduce their positions as the yen strengthened.

While this theory might be valid, no concrete data supports it. The stronger-yen/weaker-U.S.-tech trend could be coincidental. Alternatively, the yen, still holding some safe-haven status despite hitting a 38-year low, may have gained buyers due to the stock market downturn.

Regardless, the correlation was evident. Given the uncertainty around the BOJ’s policy tightening early Wednesday, the meeting in Tokyo might initially move the markets midweek.

Markets expect the interest rate gap favoring the dollar to narrow. Charu Chanana, Saxo’s head of FX strategy, notes that the BOJ has a history of disappointing hawkish expectations. The BOJ will likely tighten policy by reducing its bond-buying program. Chanana predicts it will cut purchases of 5 to 10-year notes from ¥6 trillion ($32 billion) to ¥5 trillion ($27 billion) monthly, with a further reduction to ¥3 trillion ($19.5 billion) within two years.

Traders are less certain about a rate hike from the current 0.1%. The market anticipates a 15 basis point hike with a 50% probability, implying a 7-8 basis point rise. Chanana doubts the BOJ will hike rates and significantly reduce bond buying simultaneously, noting, “Two hawkish moves at one policy meeting may be a bit of a stretch for a central bank that is inherently dovish by nature.”

Thus, the market impact of the meeting may be less severe than some expect. With the yen having rallied last week, much of the policy shift is likely priced in. Chanana believes sustained yen appreciation, with USDJPY moving below 150, is unlikely unless U.S. recession risks rise significantly or the Fed takes a sharp dovish turn.

If the BOJ does not meet hawkish expectations and signals caution, USDJPY could rise back above 155, and yen-funded carry trades could return. This would benefit Japan’s Nikkei 225 stock index, which typically moves inversely to the yen. The prospect of continued cheap money in Japan would likely support global stock market sentiment as well.