📈 From Rally to Rest: Expert Strategist Anticipates S&P 500’s Calm Waters Ahead 🛶📉

A seasoned strategist whose accurate prediction of the 2023 market rally garnered attention now envisions a period of stagnation for stocks throughout the remaining course of this year and possibly extending into 2024. This foresight is rooted in the belief that corporate earnings growth will fall short of the exceedingly optimistic expectations set by Wall Street.

Barry Bannister, an equity strategist at Stifel, has conveyed his insights in a recent report, emphasizing that the driving force behind this year’s rally – the relief stemming from the non-materialization of a U.S. recession in 2023—has likely peaked.

According to Bannister’s outlook, according to FactSet data, the S&P 500 index is poised to traverse a lateral trajectory for the rest of 2023, culminating at approximately 4,400 points, a decrease of around 68 points from its closing value on Wednesday. Nevertheless, Bannister identifies potential prospects within sectors that have lagged behind the market leaders.

His approach revolves around “pair trades,” encompassing the shorting of prominent Big Tech stocks while concurrently investing in financials, materials, industrials, and other cyclical growth stocks that have experienced subpar performance.

Bannister anticipates that the equal-weighted S&P 500 index will outperform the conventionally capitalized S&P 500 during the latter part of the year.

Recent trends have already started validating these prognostications. Since mid-July, coinciding with the commencement of the corporate earnings season, the equal-weighted S&P 500 has surged by 2.4%, surpassing the 1.6% gain achieved by the conventional S&P 500.

Within the same timeframe, several members within the “Magnificent Seven” consortium of mega-cap technology stocks, which Bannister recommends shorting, have displayed signs of retreat. Apple Inc. and Tesla Inc. have notably declined, while Nvidia Corp. remains relatively stable.

His accurate call on this year’s market resurgence underscores Banister’s forecasting prowess. While many analysts projected a slump in stocks during the first half of 2023, followed by a rebound later in the year, Bannister diverged from the norm by forecasting a reversal predicated on the anticipation of diminishing U.S. inflation.

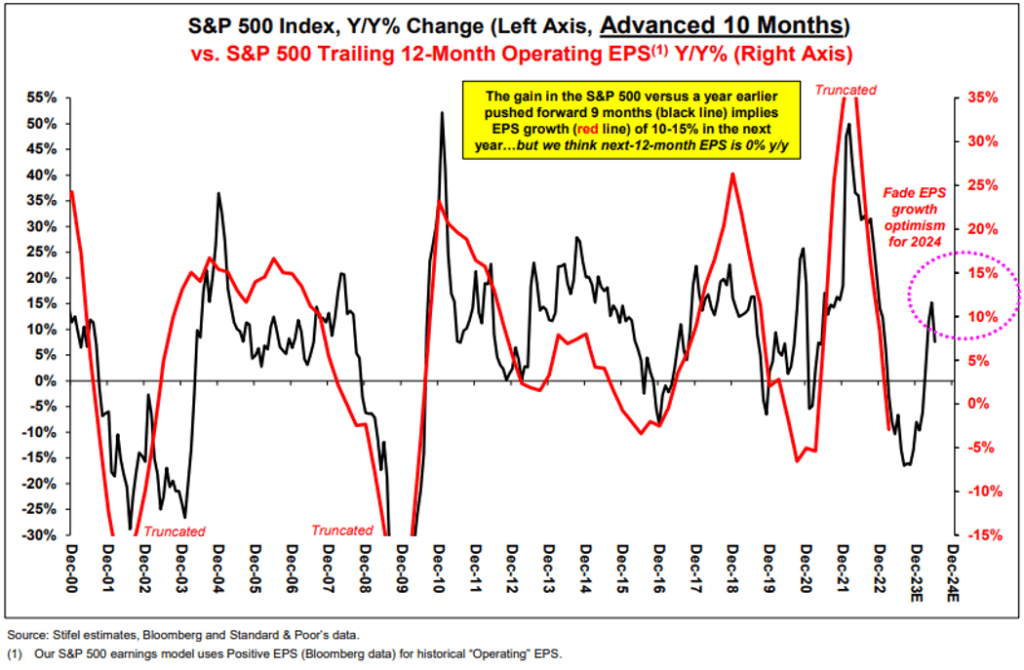

This prediction was validated as June’s Consumer Price Index (CPI) data indicated a mere 0.2% uptick in consumer prices, signifying a retreat in inflation to a pace not witnessed in two years. Bannister now posits that the deceleration in inflation is nearing its threshold. Furthermore, he contends that stocks could encounter challenges in 2024 due to Wall Street’s elevated predictions for corporate earnings growth failing to materialize.

For the upcoming year, Bannister and Stifel foresee aggregate S&P 500 earnings per share hovering around $209, a marginal departure from the 2023 projections, in contrast to the market consensus of $226.

Bannister concludes that earnings might stumble as a mild recession emerges in Q1 2024. Additionally, a rise in oil prices could trigger a minor price shock, propelling the prevailing 3% inflation to establish a new baseline. This scenario would render it intricate for the Federal Reserve to validate interest rate reductions.

In Banister’s estimation, lethargic economic expansion and the aftermath of COVID-19 stimulus measures will further cast a shadow on corporate profits.

Given the recent downtrend observed in early August, with the S&P 500, Nasdaq Composite, and Dow Jones Industrial Average registering losses, Bannister’s circumspect standpoint continues to capture attention.