The relationship between Treasury yields and the stock market is widely recognized.

The recent surge in yields was largely blamed for a market downturn, leading the S&P 500 to slide over 10% from its late July peak, falling into correction territory by the end of last month.

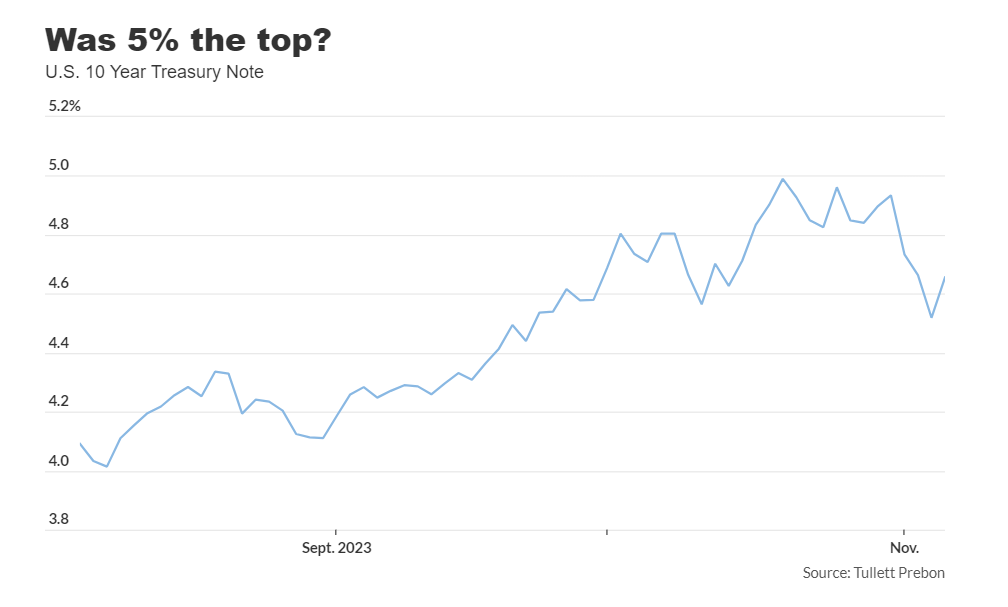

However, there was a marked shift last week. Yields on 10-year and 30-year Treasury notes saw their most significant decline since March, sparking a surge in stocks. The S&P 500, Dow Jones Industrial Average, and Nasdaq Composite recorded their most substantial weekly gains in 2023.

The week concluded with the S&P 500 closing at 4,358.34.

Investors are currently debating whether yields have hit their peak, which typically move in the opposite direction to Treasury prices. The burning question remains: will a clear peak in yields signal the revival of the 2023 stock market rally?

As is often the case in financial markets, outcomes depend largely on the context.

Analysts at U.K.-based Matrix Trade emphasized this uncertainty, noting that yields could reach a peak for various reasons, but not all outcomes would favor stocks.

One positive scenario for stocks envisions a robust economy while inflation decreases, allowing the Federal Reserve to reduce interest rates without igniting inflation reminiscent of the 1970s. However, this scenario seems improbable without a significant rise in unemployment.

Conversely, a potential recession could see yields and stocks declining simultaneously, similar to the periods of 2000-2002 and 2007-2009.

Economists have faced challenges in accurately predicting the economy’s trajectory, citing the inconsistency in forecasts. The Matrix Trade analysts highlighted the difficulty in timing signals like the inversion of the yield curve, typically a reliable indicator of an impending recession, but with uncertain timing.

To refine this signal, they suggested combining it with unemployment claims, anticipating that surpassing 250,000 first-time claims might signal a point of no return.

While the future of the stock market remains uncertain, identifying the peak in yields might be clearer.

The analysts consider the 4.33%-4.43% range as a significant inflection point for the 10-year Treasury note. Remaining within this range could mean the potential for the 10-year yield to exceed 5%. However, if this range is breached, it could indicate the end of the rally.

The analysts also suggest the possibility of a broader correction, with the 10-year yield potentially declining to 2.5% to 3%, suggesting economic pressure and a potential recession.

In summary, the current optimistic rally may face challenges, potentially hitting around 4,103 again early next year if stocks fail to continue their current momentum.

John Paul is the founder of DayTradeToWin, a trading education and software company established in 2008, supporting traders worldwide. His expertise focuses on price action-based futures trading strategies and structured market analysis.

DayTradeToWin delivers trading education, indicators, and software tools designed to help traders apply disciplined, rule-based decision-making across global futures markets.

He is the creator of multiple trading methodologies, including the Sonic System, Atlas Line, and Trade Scalper, which help traders identify structured opportunities in markets such as the E-mini S&P 500 (ES), Nasdaq (NQ), crude oil (CL), and gold (GC).

Official website: https://daytradetowin.com