S&P 500’s November Rally Rewrites History: Markets Wrap Chronicles Century’s Best Gains

The stock market on Wall Street witnessed a remarkable resurgence towards the conclusion of the day, leading to a notable uptick in November. This sudden increase was motivated by the perception that the Federal Reserve would halt its aggressive approach to raising interest rates.

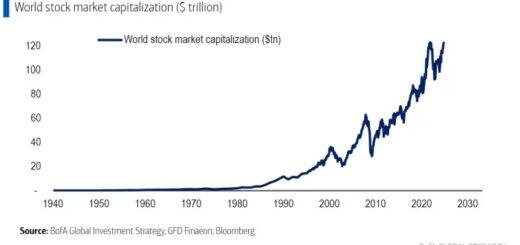

The S&P 500 has seen a significant increase of $3 trillion this month, bringing it within 5% of its highest point. In November, the leading US stock market index rose by over 8%, a rare occurrence that has happened less than 10 times in the same month since 1928, according to Bloomberg’s data. This is also the largest monthly gain for the index since July 2022. However, Treasuries declined following a strong rally, and although the dollar ended higher, it had its worst performance in a year.

Over the past couple of weeks, there has been a decline in consumer spending, inflation, and job market activity in the United States. This indicates that the rate of economic growth is slowing down gradually. The core personal consumption expenditures price index, which is an essential gauge of underlying inflation for the Federal Reserve, aligns with the forecasts made by economists.

According to Sonu Varghese, a global macro strategist at Carson Group, recent events are expected to strengthen the belief that the change in monetary policy is close at hand. It is likely that the Federal Reserve will lower interest rates at least once between January and June of 2024. The acknowledgment by Fed officials regarding the decrease in inflation, even with a strong economy and low unemployment, has laid the groundwork for the introduction of interest rate reductions.

At present, as per Callie Cox from eToro, the market is currently experiencing a bullish trend, unless there is any contrary evidence to indicate otherwise.

Powell and the presidents of the Federal Reserve are openly discussing the advancement of inflation and the potential for reducing interest rates. In industries affected by interest rates, there might be a continuous need for rate cuts if the Fed’s viewpoint remains steady. Nonetheless, it is crucial to exercise caution due to the economic slowdown and the lingering possibility of a recession.

There is good news for those who have a positive outlook on the stock market, as indicated by the Economic Regime Index model from Bloomberg Intelligence. It suggests that the United States has likely overcome its major macroeconomic obstacles.

According to Gina Martin Adams, the chief equity strategist at BI, the S&P 500 has shown positive signs as it rebounded from its lowest point in late 2022. However, the index recently entered a recession again, suggesting potential economic instability in the future. Nonetheless, as long as the index continues to stay above its previous lows, the overall outlook remains optimistic for the S&P 500.

According to Chris Verrone from Strategas, clients have been asking whether the excellent November performance would have a negative effect on the usual December Santa Claus rally. However, Verrone clarified that this is not the situation.

He observed that there is clear bias towards a significant improvement in performance during December following a disappointing display in November. Nevertheless, there is very little fluctuation in the rest of the data. Verrone mentioned that the December performance is approximately equal to the average of November, despite having achieved substantial progress in November.

Traders stayed alert in watching the recent comments made by American officials. John Williams, the President of the Federal Reserve Bank of New York, stressed that the main borrowing rate is currently at or near its peak and described the policy as “very strict”. Mary Daly, the President of the San Francisco Federal Reserve Bank, expressed belief in the current interest rates as an efficient means to control inflation. Nevertheless, she mentioned that she is not contemplating any cuts and it is too early to determine if there will be additional hikes.

According to Brian Rose, a senior economist at UBS Global Wealth Management, it is currently premature to give up on the Federal Reserve’s inclination to tighten their forward guidance. Rose expects Fed Chair Jerome Powell, who will be speaking publicly on Friday, to be cautious in order to avoid appearing overly accommodating.

Yellen is positive about a seamless shift in the economy and indicates that unemployment rates could level off.

If Powell makes more cautious remarks, the weak economic information might cause the markets to go up, which would be favorable for Jose Torres at Interactive Brokers. Nevertheless, the recent advancements only offer a moderate level of positivity because Powell has already emphasized that the Federal Reserve will only start reducing rates when there is proof of a continuous decline in inflation.

According to Torres, if he maintains a strong stance and fails to meet the anticipated interest rate cuts at the start of next year, then the current data might be comparable to a misleadingly warm day in February. Although it may give the impression that Spring is approaching, it is usually only a temporary respite from the arduous job of removing snow and wearing heavy winter clothing akin to the appearance of the Michelin tire man.

In the same way, Torres said that if Powell keeps being careful, the current pessimism about potential interest rate cuts in the near future could cause unpredictable changes in the market.

Traders were not convinced by OPEC+’s output reduction, leading to a decrease in oil prices.

Corporate Highlights:

- Tesla Inc. has successfully handed over the initial batch of futuristic Cybertrucks resembling those in the movie Blade Runner to its customers, despite encountering obstacles and setbacks in production for a duration of two years. These cutting-edge vehicles begin at a cost of $60,990, with the possibility of additional savings that Tesla anticipates could lower the final purchase price to $49,890.

- Dell Technologies Inc. released news of revenue that was unexpectedly lower than predicted, primarily caused by a consistent lack of demand from businesses for personal computers.

- Walt Disney Co. recently revealed their plans to distribute a dividend of 30 cents per share for the second half of their fiscal year, as part of their commitment to resume payment after temporarily halting it due to the pandemic.

- OpenAI is reportedly sticking to its plan of enabling its employees to sell their shares in the company via a tender offer, according to sources. Additionally, they are granting interested parties an extra month to contemplate and finalize their choices.

- Canada has opted to buy a maximum of 16 military surveillance aircraft from Boeing Co. for a total cost of $7.7 billion, rejecting a competing alternative offered by Canadian private-jet maker, Bombardier Inc.

- Ford Motor Company has changed its financial predictions and now expects to make less profit than originally anticipated. This adjustment is a result of higher labor costs stemming from the recently negotiated union agreement with the United Auto Workers.

- Nelson Peltz’s Trian Fund Management LP, a billionaire, plans on seeking representation in the board of directors at the entertainment company Walt Disney Co. after their request for seats was turned down.

- Meta Platforms Inc. has taken legal action against the US Federal Trade Commission, claiming that the commission’s internal procedures are unconstitutional. The company is requesting a court order to immediately halt the commission’s efforts to alter a privacy agreement made in 2020.

- AbbVie Inc. has recently made a deal to acquire ImmunoGen Inc. for $10.1 billion. The objective behind this purchase is to gain entry into the growing market of valuable cancer treatments.

Key events this week:

- China Caixin Manufacturing PMI, Friday

- The Eurozone’s manufacturing Purchasing Managers’ Index (PMI) data, compiled by S&P Global, was made available on Friday.

- Reports on US construction spending and the ISM Manufacturing index will be released on Friday.

- On Friday, there will be an informal discussion in Atlanta, in which Federal Reserve Chair Jerome Powell will participate.

- A speech was given by Austan Goolsbee, the President of the Chicago Federal Reserve, on Friday.

Some of the main moves in markets:

Stocks

- At 4 p.m. in New York, the S&P 500 experienced a 0.4% rise.

- The Nasdaq 100 fell 0.2%

- The Dow Jones Industrial Average rose by 1.5%.

- The MSCI World index rose 0.2%

Currencies

- There was a 0.4% rise in the Bloomberg Dollar Spot Index.

- The euro fell 0.7% to $1.0887

- The British pound fell 0.5% to $1.2626

- The Japanese yen’s worth declined by 0.7%, resulting in a ratio of 148.22 yen to one dollar.

- Cryptocurrencies

- Bitcoin was little changed at $37,757.5

- Ether rose 0.8% to $2,044.88

Bonds

- The 10-year Treasury’s interest rate rose by eight basis points to 4.34%.

- The yield on Germany’s 10-year bond rose by two basis points to reach 2.45%.

- The interest rate for a 10-year period in Britain rose by eight basis points to reach 4.18%.

Commodities

- The cost of West Texas Intermediate crude oil has decreased by 3.1%, currently standing at $75.44 per barrel.

- The value of gold decreased by 0.4%, reaching $2,035.57 per ounce.