A fascinating dynamic is unfolding in the U.S. bond and stock markets, which remain calm despite recent fluctuations in Treasury yields.

In the past two weeks, U.S. government debt rates have seen significant volatility. At the end of May, rates surged to one-month highs due to expectations that the Federal Reserve would not cut interest rates soon, unsettling the stock market. Then, last Thursday, rates dropped to their lowest levels since late March, driven by renewed concerns about a U.S. economic slowdown, marking the longest stretch of declines in a year.

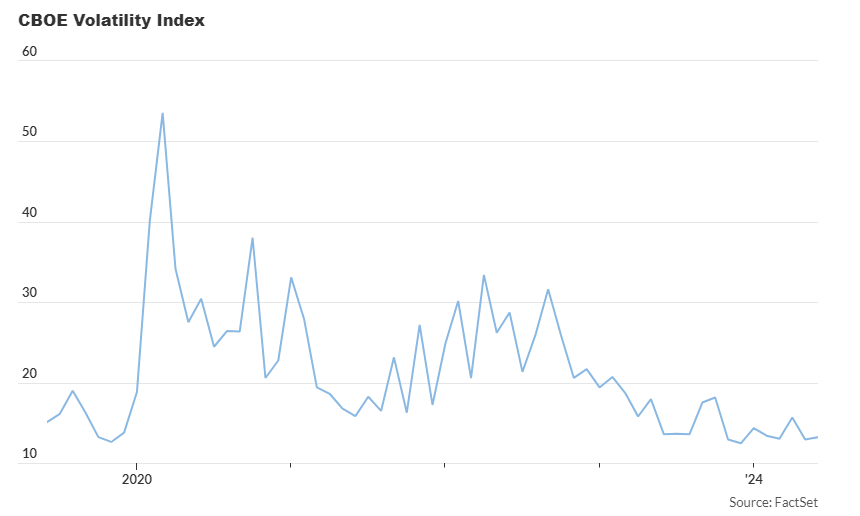

Despite these swings, overall market volatility has stayed low. This is reflected in both the ICE BofAML MOVE Index, which measures expected interest-rate volatility in the Treasury market, and the CBOE Volatility Index (VIX), which tracks expected volatility in the U.S. stock market and has barely moved this year.

The MOVE Index has also decreased from its early 2023 peaks, a period when the Federal Reserve was still raising interest rates. “In 2022 and into 2023, there was significant volatility in the Treasury market as investors tried to anticipate the Fed’s actions,” said Van Hesser, chief strategist for Kroll Bond Rating Agency. “Uncertainty around the economy’s strength and the necessary interest rates to control inflation contributed to this volatility.”

Hesser noted that as it became clearer that inflation was easing and the economy was heading towards a soft landing, volatility diminished. This relative calm persisted on Tuesday, ahead of the consumer-price index release for May and the Federal Reserve’s policy update. Treasury yields for the 2-year, 10-year, and 30-year bonds fell after a solid $39 billion 10-year auction, while U.S. stocks closed mostly higher.

“Corporate earnings growth is positive, consumer spending remains robust, and investors are optimistic about economic growth,” Hesser said. “The key question now is the future outlook. Despite ongoing uncertainty, improved visibility has dampened bond market volatility.”

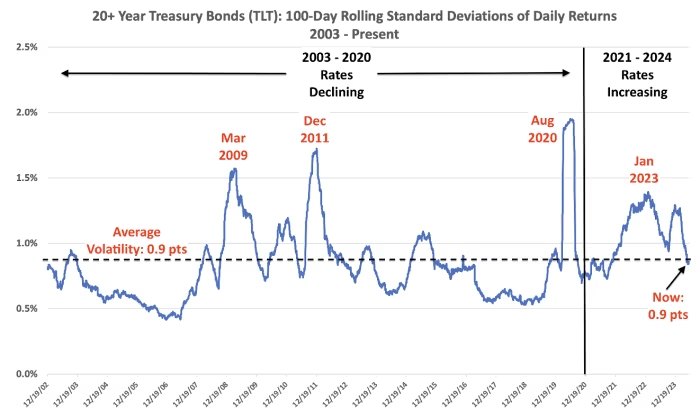

DataTrek Research co-founders Nicholas Colas and Jessica Rabe highlighted the historical price action at the long end of the U.S. government-debt yield curve, examining the 100-day standard deviation of daily returns for the iShares 20+ Year Treasury Bond ETF (TLT) from 2003 to the present. They noted that bond-market volatility typically increases significantly only during crises, which benefits bondholders.

“Current 20+ Year Treasury volatility is running at its long-term average,” Colas and Rabe wrote. “This indicates that yields are likely to remain stable until macroeconomic conditions change.”

Owning long-term Treasurys is seen as a contrarian trade that may require considerable patience before it pays off, according to Colas and Rabe.

John Paul is the founder of DayTradeToWin, a trading education and software company established in 2008, supporting traders worldwide. His expertise focuses on price action-based futures trading strategies and structured market analysis.

DayTradeToWin delivers trading education, indicators, and software tools designed to help traders apply disciplined, rule-based decision-making across global futures markets.

He is the creator of multiple trading methodologies, including the Sonic System, Atlas Line, and Trade Scalper, which help traders identify structured opportunities in markets such as the E-mini S&P 500 (ES), Nasdaq (NQ), crude oil (CL), and gold (GC).

Official website: https://daytradetowin.com