The upcoming election could fundamentally change the inflation outlook for the next three to four years, according to an inflation trader. While many investors and traders are optimistic about cooling U.S. inflation ahead of Thursday’s consumer-price index for June, Wall Street is concerned about the potential inflationary impacts of a second Trump presidency.

Before the CPI report, there are conflicting views on the future of U.S. inflation, complicating the Federal Reserve’s analysis of the appropriate path for interest rates, which remain at 23-year highs of 5.25% to 5.5%. Major U.S. stock indexes closed mostly higher on Tuesday, sending the S&P 500 and Nasdaq Composite to record closes despite a selloff in U.S. government debt that pushed up 10- and 30-year Treasury yields for the first time in five sessions.

One perspective is that inflation will likely continue easing as U.S. growth slows, allowing the Federal Reserve to cut interest rates as soon as September. Economists expect the annual headline CPI inflation rate to fall to 3.1% in June from 3.3% in May, with inflation traders predicting a drop to 2% by May 2025.

Another perspective suggests that inflation could rise again if Trump is re-elected due to his trade and immigration proposals. Parts of the market have expressed concern about Trump 2.0, as seen in a two-day rise in Treasury yields on June 28 and July 1, despite four months remaining before Americans vote.

“For good reasons, traders link Trump’s policy agenda with inflation,” said Thierry Wizman, a global FX and rates strategist at Macquarie. “They see policy rates being higher than otherwise under Trump 2.0.”

Trump leads President Joe Biden in polls nearly two weeks after their June 27 debate, drawing attention to his proposals for 10% duties on all imports and minimum 60% tariffs on Chinese goods. Biden has also faced criticism for the U.S. inflation run-up that began in 2021, following his Covid-relief plan that added $1.9 trillion in federal spending.

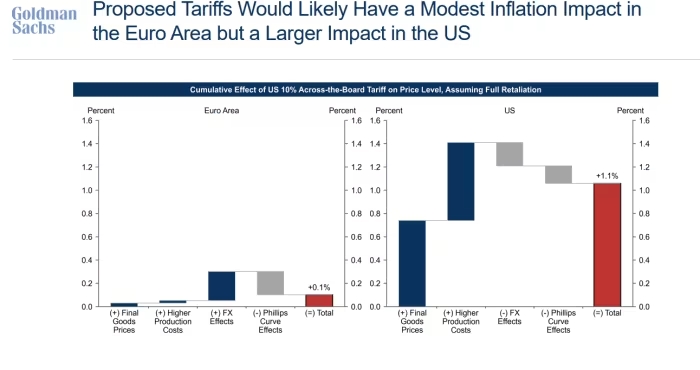

Goldman Sachs’ chief economist Jan Hatzius recently stated that Trump’s 10% tariff proposal could trigger reciprocal actions by other countries, potentially raising U.S. inflation by 1.1 percentage points and leading to five extra quarter-point rate hikes by the Fed.

Additionally, Deutsche Bank strategist Steven Zeng highlighted the impact of Trump’s immigration policies on U.S. interest rates. He noted that increased immigration flows have acted as a positive supply shock, aiding the Fed in cutting rates, and that reversing these flows could lead to higher wage inflation and a more hawkish Fed stance.

After Fed Chairman Jerome Powell’s congressional testimony on Tuesday, fed-funds futures traders priced in a 70% chance of a quarter-point rate cut by September. However, inflation trader Gang Hu of WinShore Capital Partners in New York doubts any rate cuts will occur in 2024. He emphasized that the outcome of the November 5 presidential election could drastically change everything, necessitating careful consideration by the Fed.

“Right now, it’s all about Trump. That’s the major theme and the Fed cannot ignore the possible election results at all,” Hu said. “It’s about an election that can fundamentally change the inflation picture for the next three to four years, and parts of the market are already worrying about that picture.”

The Fed’s role in controlling inflation means policymakers will likely consider Trump’s tariff proposals and immigration reforms, given their potential impact on the labor market and inflation. On Tuesday, Powell avoided discussing Trump’s tariff plans directly and instead highlighted the persistent nature of inflation after the 1970s and the current era’s supply and demand shocks from the post-Covid reopening of the U.S. economy.

“The Fed is absolutely not going to go anywhere near Trump’s policies by talking about them,” said economist Derek Tang of Monetary Policy Analytics. He suggested that the Fed will use uncertain forecasts as a reason to avoid addressing Trump-related risks ahead of the November election. Tang predicted that the Fed might start easing rates by September or December but could reverse course if needed, potentially confusing investors.

John Paul is the founder of DayTradeToWin, a trading education and software company established in 2008, supporting traders worldwide. His expertise focuses on price action-based futures trading strategies and structured market analysis.

DayTradeToWin delivers trading education, indicators, and software tools designed to help traders apply disciplined, rule-based decision-making across global futures markets.

He is the creator of multiple trading methodologies, including the Sonic System, Atlas Line, and Trade Scalper, which help traders identify structured opportunities in markets such as the E-mini S&P 500 (ES), Nasdaq (NQ), crude oil (CL), and gold (GC).

Official website: https://daytradetowin.com