S&P 500 Futures Hit Pause Button Amidst Inflation Data and Fed Minutes

Early on Wednesday, the recent surge in U.S. stock futures came to a temporary halt as market participants focused on upcoming events, including the release of inflation data and the kickoff of the corporate earnings season.

Current Activity in Stock-Index Futures:

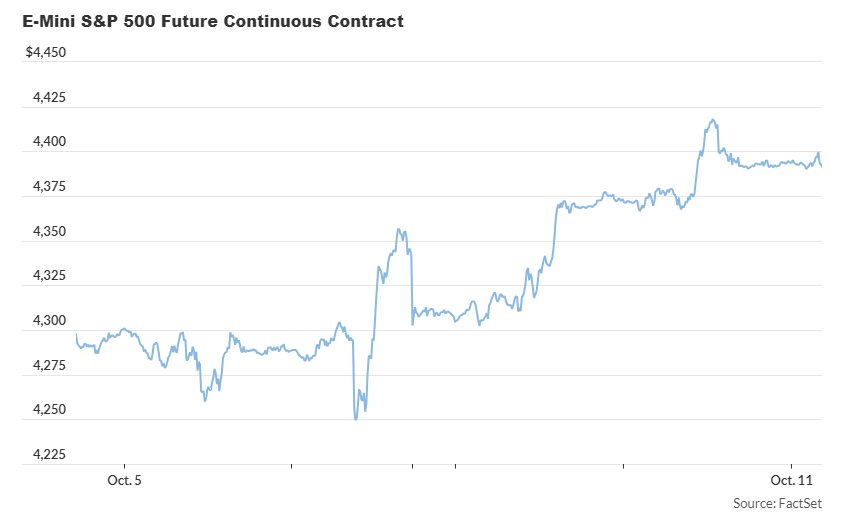

- S&P 500 futures (ES00, 0.33%) saw a modest rise of 2 points, remaining flat at 4394.

- Dow Jones Industrial Average futures (YM00, 0.31%) dipped by 2 points, staying put at 33934.

- Nasdaq 100 futures (NQ00, 0.44%) registered a gain of 22 points, marking a 0.1% uptick to reach 15292.

Recent Market Performance:

On the previous trading day, the Dow Jones Industrial Average (DJIA) witnessed a 135-point increase, equivalent to a 0.4% gain, closing at 33739. The S&P 500 (SPX) showed a 23-point climb, reflecting a 0.52% increase, closing at 4358. The Nasdaq Composite (COMP) reported a 79-point rise, marking a 0.58% increase, closing at 13563.

Driving Forces in the Market:

Over the past three trading days, the S&P 500 has enjoyed a 2.35% rise, primarily driven by a significant decline in the yield on 10-year Treasurys (BX:TMUBMUSD10Y), which receded by approximately 20 basis points from the recent 16-year peak observed last Friday.

This drop in long-term implied borrowing costs follows recent statements from Federal Reserve officials, hinting that the central bank might have concluded its cycle of interest rate increases.

Richard Hunter, Head of Markets at Interactive Investor, remarked, “Markets continued to trend upwards as the uncertainties related to the Middle Eastern conflict were mitigated by a further moderation in the Federal Reserve’s language.”

While bond yields have declined further on Wednesday, the gains in stock-index futures have been modest, with traders adopting a more cautious approach as they brace for crucial economic data releases and corporate earnings reports in the coming days.

Susannah Streeter, Head of Money and Markets at Hargreaves Lansdown, noted, “The surge in optimism, driven by hopes that the Fed will take a more lenient approach with its interest rate policies, seems to have hit a plateau. Investors are showing a bit more restraint as they look forward to tomorrow’s release of U.S. inflation data.”

On the economic front, the U.S. consumer price index report for September is scheduled for publication before the market opens on Thursday. Additionally, investors are eagerly awaiting the release of producer prices data for September at 8:30 a.m. Eastern, along with the minutes from the Federal Reserve’s previous policy meeting at 2 p.m.

Streeter emphasized that “investors are highly sensitive to data, and if U.S. inflation shows any signs of deviating from its downward trajectory, it could unsettle the markets and challenge expectations of a more dovish stance from the Federal Reserve.”

Wednesday also brings a series of speeches from Federal Reserve officials. Fed Governor Christopher Waller is expected to deliver remarks in Park City, Utah, at 10:15 a.m., Atlanta Fed President Raphael Bostic is scheduled to discuss the economic outlook at 12:15 p.m., and Boston Fed President Susan Collins will give the Goldman Lecture on Economics at Wellesley College at 4:30 p.m.

Traders are also eagerly anticipating the start of the third-quarter corporate earnings season, which kicks into high gear with major banks such as JPMorgan Chase (JPM), Citigroup (C), and Wells Fargo (WFC) set to release their earnings reports on Friday.