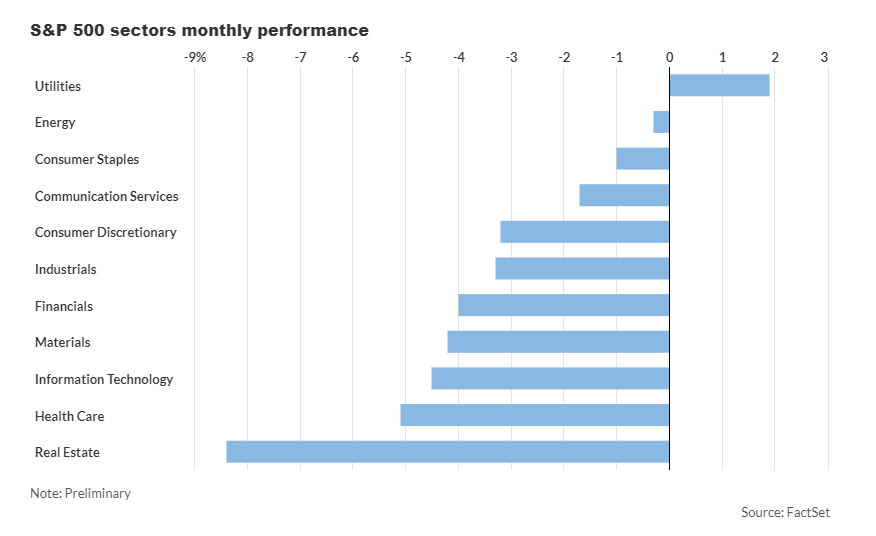

In April, U.S. stocks faced their toughest month of 2024, as ten out of the S&P 500 index’s 11 sectors saw significant declines. Both the S&P 500 index and the Nasdaq Composite experienced their first monthly drops since October, with decreases of 4.2% and 4.4% respectively. Investors grappled with concerns over persistent inflation, which tempered expectations of Federal Reserve interest-rate cuts, alongside a mix of first-quarter earnings reports and escalating tensions in the Middle East, contributing to market volatility.

The Dow Jones Industrial Average also took a hit, marking its most substantial monthly decline by percentage since September 2022, according to Dow Jones Market Data.

The real estate and healthcare sectors were among the hardest hit, with drops of 8.6% and 5.2% respectively. Real estate stocks suffered their worst month since September 2022, while the biotech, pharmaceuticals, and health insurance industries faced their most significant monthly declines since August 2022.

The technology sector, including mega-cap tech names, witnessed steep declines, dragging down the broader market from previous record highs. Specifically, the information technology and communication services sectors saw drops of 5.5% and 2.2% respectively, marking their most substantial monthly declines since fall 2023.

Meanwhile, the consumer discretionary sector fell by 4.4%, its worst month since October.

At the beginning of 2024, investors had anticipated significant interest rate cuts by the central bank to alleviate price pressures. However, a series of unexpectedly high inflation data releases in April prompted a reassessment of rate cut timing, with some investors speculating that the first reduction might not occur until September or later in the year.

This sentiment also triggered increases in Treasury bond yields alongside the U.S. dollar. The 2-year Treasury yield surged to 5.043%, its highest level since November, while the 10-year Treasury yield jumped 49.1 basis points to 4.683% in April, the most significant monthly increase since September 2022.

The ICE U.S. Dollar Index, which measures the dollar’s strength against a basket of currencies, rose for a fourth consecutive month, climbing by 1.7% in April, its best performance since January and its longest winning streak since September 2022.

Despite the overall market downturn, the utilities sector emerged as a bright spot, posting a 1.6% gain for the month. This marked the first time since October that the utilities sector was the sole monthly gainer, according to Dow Jones Market Data.

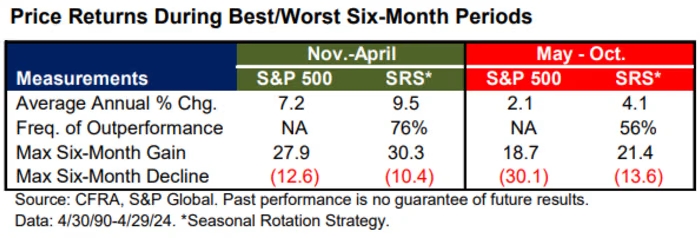

As May begins, investors ponder the wisdom of the age-old Wall Street adage, “sell in May and go away,” which suggests a weaker period for stocks until late October. However, historical data, as popularized in the Stock Trader’s Almanac, indicates that November through April typically records the highest average price change for the S&P 500, while May through October tends to see weaker returns.

Sam Stovall, chief investment strategist at CFRA Research, advises investors to consider rotating between stock sectors rather than completely exiting equity positions during this period. Historical data since 1990 suggests that sectors like consumer discretionary, industrials, materials, and technology outperform during the November-April period, while defensive sectors like consumer staples and healthcare fare better during May-October.

Stovall highlights a hypothetical portfolio that rotates between these sectors, yielding higher returns and lower volatility compared to the benchmark S&P 500 index.

John Paul is the founder of DayTradeToWin, a trading education and software company established in 2008, supporting traders worldwide. His expertise focuses on price action-based futures trading strategies and structured market analysis.

DayTradeToWin delivers trading education, indicators, and software tools designed to help traders apply disciplined, rule-based decision-making across global futures markets.

He is the creator of multiple trading methodologies, including the Sonic System, Atlas Line, and Trade Scalper, which help traders identify structured opportunities in markets such as the E-mini S&P 500 (ES), Nasdaq (NQ), crude oil (CL), and gold (GC).

Official website: https://daytradetowin.com